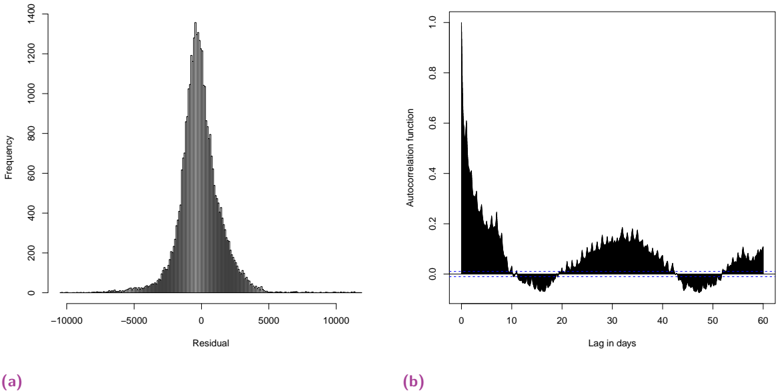

## Chart Type: Residual Histogram and Autocorrelation Function Plot

### Overview

The image presents two plots: (a) a histogram of residuals and (b) an autocorrelation function plot. The residual histogram shows the distribution of residuals, while the autocorrelation function plot shows the correlation between a time series and its lagged values.

### Components/Axes

**Plot (a): Residual Histogram**

* **Title:** Implicitly, distribution of residuals.

* **X-axis:** Residual, with values ranging from -10000 to 10000, with tick marks at -10000, -5000, 0, 5000, and 10000.

* **Y-axis:** Frequency, with values ranging from 0 to 1400, with tick marks at 0, 200, 400, 600, 800, 1000, 1200, and 1400.

**Plot (b): Autocorrelation Function Plot**

* **Title:** Autocorrelation function

* **X-axis:** Lag in days, with values ranging from 0 to 60, with tick marks at 0, 10, 20, 30, 40, 50, and 60.

* **Y-axis:** Autocorrelation function, with values ranging from 0.0 to 1.0, with tick marks at 0.0, 0.2, 0.4, 0.6, 0.8, and 1.0.

* A horizontal dashed blue line is present at approximately y = 0.0.

### Detailed Analysis

**Plot (a): Residual Histogram**

* The histogram is centered around 0.

* The distribution appears approximately normal, with a peak frequency of approximately 1300 near 0.

* The frequency decreases as the absolute value of the residual increases.

* The distribution is symmetric around 0.

**Plot (b): Autocorrelation Function Plot**

* The autocorrelation is 1.0 at lag 0.

* The autocorrelation decreases rapidly as the lag increases from 0 to approximately 5 days.

* The autocorrelation becomes negative around a lag of 10 days.

* The autocorrelation oscillates between positive and negative values as the lag increases, with decreasing amplitude.

* There are peaks in the autocorrelation around lags of 30 and 60 days.

### Key Observations

* The residual histogram suggests that the residuals are normally distributed.

* The autocorrelation function plot suggests that there is some autocorrelation in the time series, particularly at short lags.

* The oscillations in the autocorrelation function plot suggest that there may be some seasonality in the time series.

### Interpretation

The residual histogram and autocorrelation function plot provide information about the properties of the residuals from a time series model. The approximately normal distribution of the residuals suggests that the model is a good fit for the data. The autocorrelation function plot suggests that there may be some autocorrelation in the time series, which could be due to seasonality or other factors. The presence of autocorrelation in the residuals indicates that the model could be improved by including additional terms to account for the autocorrelation.