## Document Analysis: Tax Liability and Unrecognized Tax Benefits

### Overview

The image presents a snippet from a document, likely related to financial reporting and tax liability analysis. It includes a passage summarizing changes in unrecognized tax benefits, a question regarding the relationship between amounts decreasing the effective tax rate and goodwill, and a comparison of a "Gold Program" answer with a "ZS-FinDSL" reasoning and program execution.

### Components/Axes

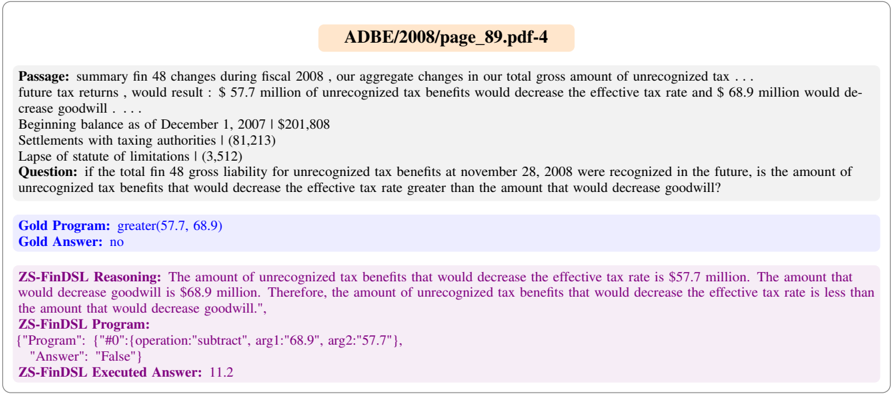

* **Header:** "ADBE/2008/page\_89.pdf-4"

* **Passage:** A summary of financial changes during fiscal year 2008 related to unrecognized tax benefits.

* **Question:** A query about the relative amounts of unrecognized tax benefits affecting the effective tax rate and goodwill.

* **Gold Program:** A program that compares 57.7 and 68.9.

* **Gold Answer:** The answer provided by the "Gold Program," which is "no."

* **ZS-FinDSL Reasoning:** The reasoning provided by the ZS-FinDSL system.

* **ZS-FinDSL Program:** The program code used by the ZS-FinDSL system.

* **ZS-FinDSL Executed Answer:** The numerical result of the ZS-FinDSL program execution, which is 11.2.

### Detailed Analysis or Content Details

* **Passage:**

* Summary of fin 48 changes during fiscal 2008.

* Aggregate changes in the total gross amount of unrecognized tax.

* $57.7 million of unrecognized tax benefits would decrease the effective tax rate.

* $68.9 million would decrease goodwill.

* Beginning balance as of December 1, 2007: $201,808

* Settlements with taxing authorities: (81,213)

* Lapse of statute of limitations: (3,512)

* **Question:**

* Asks if the amount of unrecognized tax benefits that would decrease the effective tax rate is greater than the amount that would decrease goodwill.

* **Gold Program:**

* `greater(57.7, 68.9)`

* **Gold Answer:**

* `no`

* **ZS-FinDSL Reasoning:**

* States that $57.7 million would decrease the effective tax rate.

* States that $68.9 million would decrease goodwill.

* Concludes that the amount decreasing the effective tax rate is less than the amount decreasing goodwill.

* **ZS-FinDSL Program:**

* `{"Program": ["#0": {operation:"subtract", arg1:"68.9", arg2:"57.7"}, "Answer": "False"}`

* **ZS-FinDSL Executed Answer:**

* `11.2`

### Key Observations

* The passage provides financial data related to unrecognized tax benefits and their impact on the effective tax rate and goodwill.

* The question seeks to compare the magnitudes of these impacts.

* The "Gold Program" directly compares the two amounts (57.7 and 68.9) and returns "no," indicating that 57.7 is not greater than 68.9.

* The "ZS-FinDSL" system provides reasoning consistent with the "Gold Program" and executes a subtraction operation (68.9 - 57.7), resulting in 11.2.

* The ZS-FinDSL program also returns "False" as an answer, which is not consistent with the numerical result of 11.2.

### Interpretation

The document snippet presents a scenario involving the analysis of unrecognized tax benefits and their impact on financial statements. The "Gold Program" and "ZS-FinDSL" system are used to evaluate a specific question about the relative magnitudes of the impact on the effective tax rate and goodwill.

The "Gold Program" provides a direct comparison, while the "ZS-FinDSL" system offers a more detailed reasoning and program execution. The ZS-FinDSL program calculates the difference between the two amounts, resulting in 11.2. However, the ZS-FinDSL program also returns "False" as an answer, which is inconsistent with the numerical result of 11.2. This suggests a potential error or misinterpretation in the ZS-FinDSL program's logic.

The data suggests that the amount decreasing goodwill ($68.9 million) is greater than the amount decreasing the effective tax rate ($57.7 million). The ZS-FinDSL's subtraction confirms this difference numerically.