## Chart: Regret and Expected Mean Rewards Comparison

### Overview

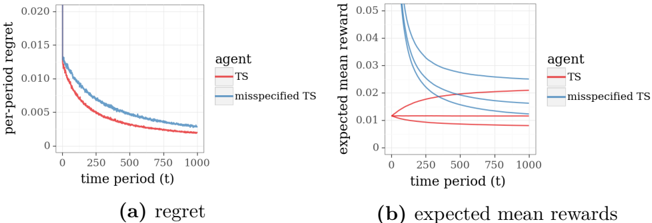

The image presents two line charts comparing the performance of two agents, "TS" (Thompson Sampling) and "misspecified TS," over time. The left chart (a) displays the per-period regret, while the right chart (b) shows the expected mean reward. Both charts share the same x-axis representing "time period (t)" from 0 to 1000.

### Components/Axes

**Chart (a): Regret**

* **Y-axis:** "per-period regret," ranging from 0 to 0.020 with increments of 0.005.

* **X-axis:** "time period (t)," ranging from 0 to 1000 with increments of 250.

* **Legend (top-right):**

* Red line: "TS"

* Blue line: "misspecified TS"

**Chart (b): Expected Mean Rewards**

* **Y-axis:** "expected mean reward," ranging from 0 to 0.05 with increments of 0.01.

* **X-axis:** "time period (t)," ranging from 0 to 1000 with increments of 250.

* **Legend (top-right):**

* Red line: "TS"

* Blue line: "misspecified TS"

### Detailed Analysis

**Chart (a): Regret**

* **TS (Red):** The per-period regret starts at approximately 0.012 and decreases over time, approaching a value around 0.002 after 1000 time periods. The decline is steeper initially and then flattens out.

* **Misspecified TS (Blue):** The per-period regret starts at approximately 0.014 and also decreases over time, approaching a value around 0.004 after 1000 time periods. The decline is steeper initially and then flattens out. The regret for misspecified TS is consistently higher than that of TS.

**Chart (b): Expected Mean Rewards**

* **TS (Red):** There are two red lines. One starts at approximately 0.012 and decreases slightly to around 0.011. The other starts at approximately 0.01 and increases slightly to around 0.012.

* **Misspecified TS (Blue):** There are two blue lines. One starts at approximately 0.01 and increases sharply to approximately 0.025, then increases more slowly to approximately 0.027. The other starts at approximately 0.05 and decreases sharply to approximately 0.02, then decreases more slowly to approximately 0.017.

### Key Observations

* In the regret chart, both agents show a decreasing trend in per-period regret over time, with the "TS" agent consistently exhibiting lower regret than the "misspecified TS" agent.

* In the expected mean rewards chart, the "TS" agent's reward remains relatively stable, while the "misspecified TS" agent's reward shows more significant fluctuations, with one line increasing and the other decreasing.

### Interpretation

The data suggests that the "TS" agent performs better in terms of minimizing regret compared to the "misspecified TS" agent. The "TS" agent also demonstrates more stable expected mean rewards. The "misspecified TS" agent, while initially having higher expected mean rewards, experiences more volatility and ultimately converges to a lower reward level than its initial peak. This indicates that the "TS" agent is more robust and efficient in this scenario. The "misspecified TS" agent's performance is likely affected by the model misspecification, leading to higher regret and unstable rewards.