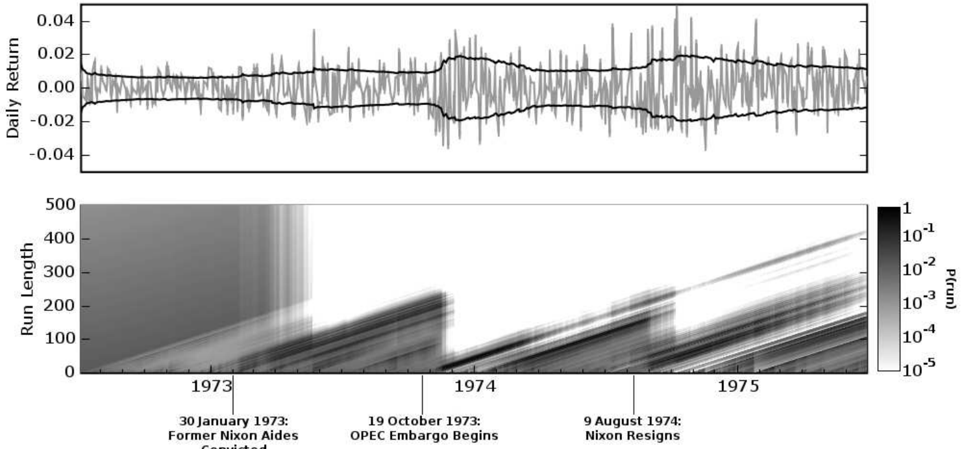

## Line Chart with Heatmap: Market Volatility and Run Length Analysis (1973-1975)

### Overview

The image contains two primary components:

1. A **line chart** titled "Daily Return" showing daily returns over time.

2. A **heatmap** labeled "Run Length" with a color scale representing probability (P(run)).

Both components are temporally aligned, spanning 1973–1975, with key historical events annotated.

---

### Components/Axes

#### Line Chart (Top)

- **Y-axis**: "Daily Return" (range: -0.04 to 0.04).

- **X-axis**: Implicit time axis (1973–1975), unlabeled but aligned with the heatmap.

- **Legend**: A single black line representing daily returns.

#### Heatmap (Bottom)

- **Y-axis**: "Run Length" (0 to 500).

- **X-axis**: Time (1973–1975), with vertical markers for:

- 30 January 1973: "Former Nixon Aides"

- 19 October 1973: "OPEC Embargo Begins"

- 9 August 1974: "Nixon Resigns"

- **Color Scale**: Right-hand gradient from white (10⁻⁵) to black (1), labeled "P(run)".

---

### Detailed Analysis

#### Line Chart Trends

- The black line fluctuates around **zero**, with peaks reaching ±0.03 and troughs near ±0.02.

- Notable volatility spikes occur around **1973–1974**, particularly near the OPEC embargo date (19 October 1973).

- Post-1974, returns stabilize closer to zero, with reduced amplitude.

#### Heatmap Patterns

- **Color Intensity**: Darker regions (higher P(run)) cluster near the bottom-left (1973) and along diagonal bands ascending to the top-right (1975).

- **Run Length**:

- Sharp increases in run length (up to ~400) occur after the OPEC embargo (19 October 1973).

- A secondary peak (~300) aligns with Nixon’s resignation (9 August 1974).

- **Probability Gradient**: The darkest areas (P(run) ≈ 1) are concentrated in the lower-left quadrant, suggesting higher probabilities of shorter run lengths in early 1973.

---

### Key Observations

1. **Event Correlation**:

- The OPEC embargo (19 October 1973) coincides with a sharp rise in run length and daily return volatility.

- Nixon’s resignation (9 August 1974) correlates with a secondary run-length peak and reduced return volatility.

2. **Probability Dynamics**:

- Higher probabilities (darker shades) of longer run lengths emerge post-1973, peaking in 1975.

- The heatmap’s diagonal bands suggest a gradual increase in run length over time, independent of daily return fluctuations.

---

### Interpretation

- **Market Volatility**: The line chart indicates that daily returns were most volatile during the OPEC embargo period, likely reflecting geopolitical/economic uncertainty. Post-1974 stability may correlate with reduced macroeconomic shocks.

- **Run Length Significance**: The heatmap’s run-length increases suggest prolonged market states (e.g., bull/bear runs) became more common after 1973, possibly due to policy shifts (e.g., Nixon’s resignation altering regulatory frameworks).

- **Anomalies**: The abrupt drop in run length in early 1973 (dark vertical band) may reflect a market reset following Nixon’s aides’ departure, preceding the OPEC shock.

The data implies that political and economic events in the early 1970s significantly influenced both short-term market returns and long-term market behavior patterns. The heatmap’s diagonal trend highlights a systemic shift toward longer market runs by 1975, potentially linked to post-Nixon policy adjustments.