# On Bitcoin Price Prediction

On Bitcoin Price Prediction

Grégory Bournassenko gregory.bournassenko@etu.u-paris.fr

Université Paris Cité

In recent years, cryptocurrencies have attracted growing attention from both private investors and institutions. Among them, Bitcoin stands out for its impressive volatility and widespread influence. This paper explores the predictability of Bitcoin’s price movements, drawing a parallel with traditional financial markets. We examine whether the cryptocurrency market operates under the efficient market hypothesis (EMH) or if inefficiencies still allow opportunities for arbitrage. Our methodology combines theoretical reviews, empirical analyses, machine learning approaches, and time series modeling to assess the extent to which Bitcoin’s price can be predicted. We find that while, in general, the Bitcoin market tends toward efficiency, specific conditions, including information asymmetries and behavioral anomalies, occasionally create exploitable inefficiencies. However, these opportunities remain difficult to systematically identify and leverage. Our findings have implications for both investors and policymakers, particularly regarding the regulation of cryptocurrency brokers and derivatives markets. Contents

1. 1 Introduction

1. 2 The Cryptocurrency Market is Efficient

1. 2.1 Eugene Fama and the Notion of No Arbitrage Opportunities

1. 2.1.1 Efficient Market Hypothesis Adaptation to Cryptocurrencies

1. 2.1.2 Random Walk and Martingale

1. 2.1.3 Cryptocurrencies and Fundamental Value

1. 2.2 From Louis Bachelier to Contemporary Models

1. 2.2.1 Modeling of Traditional Finance

1. 2.2.2 Modeling Crypto-Finance

1. 2.3 Time Series Studies and Analyses

1. 2.3.1 Fundamental Analysis

1. 2.3.2 Chartist / Technical Analysis

1. 2.3.3 Machine Learning

1. 3 The Cryptocurrency Market is Inefficient

1. 3.1 Robert Shiller and the Notion of an Inefficient Market in Terms of Arbitrage

1. 3.1.1 Volatility and Expected Dividends

1. 3.1.2 Behavioral Finance and Market Anomalies

1. 3.1.3 Speculative Bubbles

1. 3.2 Informational Inefficiency

1. 3.2.1 Market Manipulation

1. 3.2.2 Pump & Dump

1. 3.2.3 Natural Language Processing

1. 3.3 Operational Inefficiency

1. 3.3.1 At the Macroscopic Scale

1. 3.3.2 At the Mesoscopic Scale

1. 3.3.3 At the Microscopic Scale

1. 4 Conclusion

1. A isRandomBetter( $\Omega,n,k$ )

1. B isSMABetter( $\Omega,n,r$ )

1. C getHoldReturn(asset)

1. D getSMAReturn(asset, n, r)

1. E getRandomReturn(asset)

1. F getRandomPerc( $\Omega$ )

1. G getAverageAccuracy( $\Omega,n$ )

1. H NLP Trading Bot

List of Figures

1. 1 Introduction

1. 3 $\blacktriangle 9,000\%$ BTC/USD [2014-2022]

1. 2.1 Eugene Fama and the Notion of No Arbitrage Opportunities

1. 6 $\blacktriangle 14,000\%$ DOGE/USD [01/2021-05/2021]

1. 2.1.1 Efficient Market Hypothesis Adaptation to Cryptocurrencies

1. 9 $\blacktriangle 150\%$ BTC/USD [13/06/2017-01/09/2017]

1. 10 $\blacktriangledown 15\%$ BTC/USD [16/01/2018-17/01/2018]

1. 11 $\blacktriangledown 22\%$ BTC/USD [14/04/2021-25/04/2021]

1. 12 Correlation between BTC/USD, GOLD/USD, and S&P500

1. 13 S&P500 over the period available with BTC/USD

1. 14 GOLD/USD over the period available with BTC/USD

1. 2.1.3 Cryptocurrencies and Fundamental Value

1. 2.2.1 Modeling of Traditional Finance

1. 2.2.1 Modeling of Traditional Finance

1. 21 RSI Signals for BTC/USD

1. 22 SAR Signals for BTC/USD

1. 2.3.3 Machine Learning

1. 2.3.3 Machine Learning

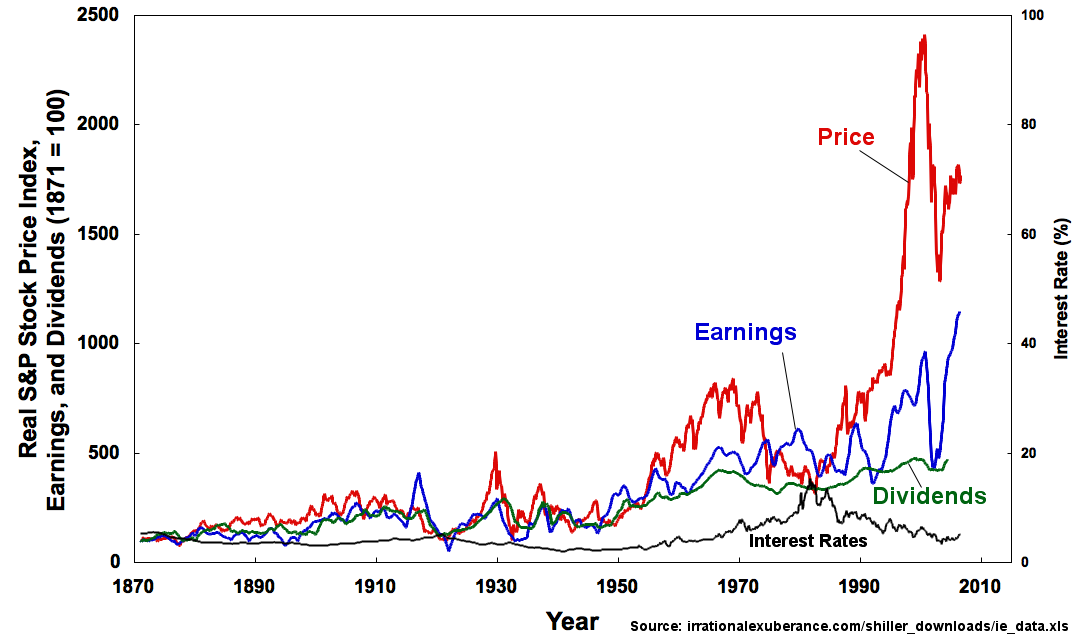

1. 27 Results of the ARIMA model

1. 28 Evolution of the S&P500 and dividends

1. 29 Results from the NLP trading bot

List of Tables

1. 1 Results of isRandomBetter( $\Omega,n,k$ )

1. 2 Results of isSMABetter( $\Omega,n,r$ )

1 Introduction

The price of Bitcoin has lost almost 50% of its value since last November, almost as much as Orpea’s stock value after its scandal. In Orpea’s case, the correlation is clear with the scandal, but for Bitcoin, such irrational volatility is rather usual.

<details>

<summary>extracted/6391907/images/btc-new.png Details</summary>

### Visual Description

## Candlestick Chart: Price Fluctuation Over Time

### Overview

The image presents a candlestick chart illustrating price fluctuations over time. The chart spans from October 2021 to April 2022. The y-axis represents price in thousands (k), ranging from 30k to 70k. The x-axis represents time, marked by months. The chart uses candlestick patterns (red and green) to indicate price movements within each period.

### Components/Axes

* **Y-Axis (Price):** Ranges from 30k to 70k, with increments of 5k.

* **X-Axis (Time):** Labeled with months: Oct 2021, Nov 2021, Dec 2021, Jan 2022, Feb 2022, Mar 2022, Apr 2022.

* **Candlesticks:** Each candlestick represents a period (likely a day or week).

* **Green Candlesticks:** Indicate a price increase during the period (closing price higher than opening price).

* **Red Candlesticks:** Indicate a price decrease during the period (closing price lower than opening price).

### Detailed Analysis

* **October 2021:** Starts around 47k, shows an upward trend, reaching approximately 62k by the end of the month.

* **November 2021:** Continues the upward trend, peaking around 67k in the middle of the month, then fluctuating between 60k and 65k.

* **December 2021:** Shows a significant downward trend, dropping from around 60k to approximately 47k.

* **January 2022:** Continues the downward trend, fluctuating between 40k and 50k.

* **February 2022:** Reaches a low point around 35k, then shows an upward trend towards the end of the month, reaching approximately 45k.

* **March 2022:** Fluctuates between 40k and 45k, with some upward spikes.

* **April 2022:** Shows a slight downward trend, starting around 45k and ending around 38k.

### Key Observations

* **Peak:** The highest price point is observed in November 2021, around 67k.

* **Lowest Point:** The lowest price point is observed in February 2022, around 35k.

* **Volatility:** The period from October 2021 to December 2021 shows high volatility, with significant price swings.

* **Downward Trend:** A clear downward trend is visible from December 2021 to February 2022.

* **Recovery:** A slight recovery is observed from February 2022 to March 2022, followed by a slight decline in April 2022.

### Interpretation

The candlestick chart illustrates the price dynamics of an asset over a seven-month period. The initial upward trend in October and November 2021 suggests a bullish market sentiment. However, the subsequent decline from December 2021 to February 2022 indicates a shift towards a bearish market. The recovery in late February and March 2022 suggests a potential stabilization or a weak bullish reversal, but the slight decline in April 2022 indicates continued uncertainty. The chart highlights the importance of monitoring price trends and volatility to understand market sentiment and make informed decisions.

</details>

Figure 1: $\blacktriangledown 50\%$ BTC/USD [11/2021-02/2022]

<details>

<summary>extracted/6391907/images/orpea-new.png Details</summary>

### Visual Description

## Candlestick Chart: Stock Price Over Time

### Overview

The image is a candlestick chart showing the price fluctuations of a stock or asset over time, from December 2021 to April 2022. The chart uses red and green candlesticks to represent price decreases and increases, respectively, within each time period.

### Components/Axes

* **Y-axis (Vertical):** Represents the price, ranging from approximately 20 to 120. Gridlines are present at intervals of 20.

* **X-axis (Horizontal):** Represents time, with labels for December 2021, January 2022, February 2022, March 2022, and April 2022.

* **Candlesticks:** Each candlestick represents a specific time period.

* **Green Candlesticks:** Indicate that the closing price was higher than the opening price.

* **Red Candlesticks:** Indicate that the closing price was lower than the opening price.

* The body of the candlestick represents the range between the opening and closing prices.

* The "wicks" or lines extending above and below the body represent the highest and lowest prices during that period.

### Detailed Analysis

* **December 2021 - January 2022:** The price fluctuates around 80-90, with both red and green candlesticks indicating periods of increase and decrease. The price appears relatively stable during this period.

* **Late January 2022 - Early February 2022:** There is a significant drop in price. A large red candlestick indicates a substantial decrease in price within a single period. The price falls from approximately 80 to around 40.

* **February 2022 - April 2022:** The price remains relatively stable, fluctuating between approximately 30 and 40. There are both red and green candlesticks, but the overall trend is sideways with a slight downward drift.

### Key Observations

* **Significant Price Drop:** The most notable event is the sharp price decrease between late January and early February 2022.

* **Volatility:** The period from December 2021 to January 2022 shows more volatility compared to the period from February 2022 to April 2022.

* **Sideways Trend:** After the price drop, the stock enters a sideways trend with relatively small price fluctuations.

### Interpretation

The candlestick chart illustrates the price movement of an asset over a five-month period. The initial stability gives way to a sharp decline, followed by a period of low volatility and sideways movement. This could indicate a significant event or change in market sentiment that impacted the asset's value. The subsequent stabilization suggests that the market has adjusted to the new price level, but there is no clear indication of a recovery.

</details>

Figure 2: $\blacktriangledown 50\%$ ORP [01/2022-03/2022]

The notion of prediction is vague, especially regarding price prediction: isn’t price itself the result of agents’ predictions about the value of an asset? Are we therefore predicting a prediction? For simplicity, we will use the term prediction as defined by American economist Alfred Cowles in his paper [Cowles 3rd, 1933], particularly in the second part, where he analyzes the reliability of "forecasters" on stock market volatility. Bitcoin, for its part, is a decentralized cryptocurrency, created in 2008, based on a "proof of work" mining protocol and a robust transaction system as explained by Satoshi Nakamoto [Nakamoto, 2008].

<details>

<summary>extracted/6391907/images/btc-new2.png Details</summary>

### Visual Description

## Line Chart: Bitcoin Price Over Time

### Overview

The image is a line chart showing the price of Bitcoin over time, from 2015 to 2022. The chart displays the price fluctuations in Bitcoin, with significant increases and decreases over the years. The chart uses two lines, one green and one red, which appear to overlap closely, suggesting they represent similar data or perhaps high and low values for each day.

### Components/Axes

* **X-axis:** Represents time, labeled with years from 2015 to 2022.

* **Y-axis:** Represents the price of Bitcoin, with values ranging from 0 to 70k (presumably USD). The scale is marked at intervals of 10k (0, 10k, 20k, 30k, 40k, 50k, 60k, 70k).

* **Data Series:** Two lines, one green and one red, that closely follow each other, indicating the price fluctuations. There is no explicit legend, but the lines likely represent daily high and low prices.

### Detailed Analysis

* **2015-2017:** The price remains relatively stable and close to 0.

* **2017-2018:** A significant increase occurs, peaking around 20k in early 2018, followed by a sharp decline.

* **2018-2020:** The price fluctuates between approximately 5k and 10k.

* **2020-2021:** A massive surge begins in late 2020, reaching a peak of approximately 65k-70k in 2021.

* **2021-2022:** The price experiences high volatility, with multiple peaks and dips, generally trending downward from the 2021 high. The price ends around 40k in 2022.

**Specific Data Points (Approximate):**

* **2015:** Price near 0.

* **Early 2018:** Peak around 20k.

* **2019-2020:** Fluctuating between 5k and 10k.

* **Late 2021:** Peak around 65k-70k.

* **2022:** Ends around 40k.

### Key Observations

* The most significant price increase occurred between 2020 and 2021.

* The price is highly volatile, especially after 2020.

* The green and red lines are very close, suggesting they represent a daily range.

### Interpretation

The chart illustrates the dramatic rise and fall of Bitcoin's price over a relatively short period. The initial stability from 2015-2017 is followed by periods of rapid growth and subsequent corrections. The volatility observed after 2020 indicates a more mature, yet still highly speculative, market. The close proximity of the green and red lines suggests that while the price fluctuates daily, the overall trend is consistent. The data suggests that Bitcoin is a high-risk, high-reward investment, subject to significant market fluctuations.

</details>

Figure 3: $\blacktriangle 9,000\%$ BTC/USD [2014-2022]

As shown above, Bitcoin has progressively gained success: initially used for anonymous transactions on illegal markets, it became a speculative tool for individuals, and eventually attracted institutional interest, despite limited daily usage [Baur et al., 2015]. Notably, Bitcoin’s underlying technology, Blockchain, was actually invented by researchers Haber and Stornetta [Haber and Stornetta, 1990], not Nakamoto, although Nakamoto was the first to apply it at large scale.

The literature on cryptocurrency prediction remains relatively poor, given the recent emergence of the technology. Virtually no academic papers referenced cryptocurrencies before 2008. Instead, much research focuses on machine learning techniques for cryptocurrency prediction. However, similarities with financial markets exist (closer to forex than stocks due to the monetary nature of cryptocurrencies), a domain extensively studied since the early 1900s. From Louis Bachelier’s Gaussian model [Bachelier, 1900] to Mathieu Rosenbaum’s rough Heston model [Gatheral et al., 2018], and Gordon-Shapiro’s valuation model [Gordon and Shapiro, 1956], numerous theories have been proposed. Yet, debates persist regarding market behavior.

According to Eugene Fama [Fama, 1970], a rational market cannot be systematically beaten. Louis Bachelier [Bachelier, 1900] states, "The determination of these activities depends on an infinite number of factors: therefore, a precise mathematical forecast is absolutely impossible." Nevertheless, Keynes [Keynes, 1937] compared the market to a beauty contest: predicting what the majority will find beautiful, not objective beauty itself. This idea echoes momentum strategies and aligns with Charles Dow’s technical analysis [Brown et al., 1998].

Alternatively, Warren Buffett promotes stock-picking and value investing, diverging from Markowitz’s modern portfolio theory [Steinbach, 2001]. However, Buffett’s method, focusing on selecting promising assets, differs from our study, where the asset (Bitcoin) is preselected. Burton Malkiel [Malkiel, 2003] famously claimed that "a blindfolded monkey throwing darts at a newspaper’s financial pages could perform as well as professional investors," although empirical studies [Pernagallo and Torrisi, 2020] challenge this assertion.

To explore random versus selected portfolios, we define a Python function isRandomBetter( $\Omega,n,k$ ) (code in Appendix A). Results:

| 1 | 141 | 998 | 10 | 10 | 20% | False |

| --- | --- | --- | --- | --- | --- | --- |

| 2 | 141 | 998 | 10 | 20 | 30% | False |

| 3 | 141 | 998 | 20 | 10 | 40% | False |

| 4 | 141 | 998 | 20 | 20 | 30% | False |

| 5 | 141 | 998 | 20 | 30 | 60% | True |

| 6 | 141 | 998 | 30 | 20 | 57% | True |

| 7 | 141 | 998 | 30 | 30 | 47% | False |

| 8 | 141 | 998 | 30 | 10 | 27% | False |

| 9 | 141 | 998 | 10 | 30 | 20% | False |

| 10 | 141 | 998 | 40 | 5 | 25% | False |

Table 1: Results of isRandomBetter( $\Omega,n,k$ )

Choosing a random crypto portfolio in 2021 was not optimal.

We will investigate whether Bitcoin price predictability depends on market efficiency. Given the cryptocurrency market’s heterogeneity, various scenarios (competitive markets, manipulated markets, rational/irrational agents) are expected.

We will show that, by default, the crypto market tends to be efficient, although inefficiencies sometimes appear, albeit difficult to exploit systematically.

We will address prediction methods under efficient market conditions, focusing on time series analysis and machine learning algorithms. We will also study prediction under inefficiency contexts, emphasizing empirical observations and stylized facts.

Let’s first examine the case when the market is efficient.

2 The Cryptocurrency Market is Efficient

We first assume an efficient market. We will explain the concept’s origins, assumptions, verify some of them, discuss model evolutions, and their implications for cryptocurrencies. We will also analyze this through machine learning and quantitative techniques, reflecting critically on the results.

2.1 Eugene Fama and the Notion of No Arbitrage Opportunities

We start with Fama’s [Fama, 1970] definition of efficient markets, comparing the US stock market and cryptocurrencies. Fama’s idea implies no arbitrage opportunities. However, as we will see later, arbitrage is relatively common in crypto markets (price differences between brokers).

<details>

<summary>extracted/6391907/images/arb1.png Details</summary>

### Visual Description

## Website Landing Page: KoinKnight

### Overview

The image is a landing page for a service called KoinKnight, which provides personal assistance for cryptocurrency arbitrage. The page features a headline, a brief description of the service, calls to action, and a stylized illustration.

### Components/Axes

* **Header:** Contains the KoinKnight logo, navigation links (Pricing, API Services, Crypto Analytics, Refer & Earn), a language selector (English), and login/signup buttons.

* **Main Content:** Features the headline "Your personal assistance for cryptocurrency arbitrage," a descriptive paragraph, and two buttons: "Try for free" and "View Demo."

* **Footer:** A small line of text: "Already using KoinKnight? Log in"

* **Illustration:** A stylized illustration of a laptop displaying data tables, a calculator, and a yellow circle.

### Detailed Analysis or ### Content Details

* **Headline:** "Your personal assistance for cryptocurrency arbitrage"

* **Description:** "Find the best trade and arbitrage opportunities using KoinKnight's powerful algorithm and real-time data exploration tools."

* **Buttons:**

* "Try for free"

* "View Demo"

* **Footer Text:** "Already using KoinKnight? Log in"

* **Navigation Links:**

* Pricing

* API Services

* Crypto Analytics

* Refer & Earn

* **Illustration Details:**

* Laptop screen displays data tables with red and green horizontal bars.

* A calculator is present.

* A yellow circle is present.

### Key Observations

* The landing page focuses on cryptocurrency arbitrage.

* The service emphasizes the use of a powerful algorithm and real-time data exploration tools.

* The design is clean and modern.

### Interpretation

The landing page aims to attract users interested in cryptocurrency arbitrage by highlighting the benefits of using KoinKnight's algorithm and tools. The "Try for free" and "View Demo" buttons encourage potential users to explore the service further. The illustration visually represents the data-driven nature of the service. The overall message is that KoinKnight provides a user-friendly and effective solution for cryptocurrency arbitrage.

</details>

Figure 4: KoinKnight

<details>

<summary>extracted/6391907/images/arb2.png Details</summary>

### Visual Description

## Website Screenshot: ArbiTool Landing Page

### Overview

The image is a screenshot of the ArbiTool website landing page. It features a modern design with a purple and blue color scheme, geometric shapes, and isometric illustrations. The page promotes a tool that identifies cryptocurrency arbitrage opportunities.

### Components/Axes

* **Header:** Contains the ArbiTool logo, navigation links (Home, About ArbiTool, Tutorial, Pricing, Arbitrage Course, Join Our Community, FAQ's, Contact), language selector (UK flag), and login/signup buttons.

* **Main Content:** Includes a headline, a brief description of the tool's functionality, call-to-action buttons, and an isometric illustration depicting cryptocurrency trading and analysis.

* **Footer:** Contains a section for trading tokens and the Altilly logo.

* **Chat Widget:** Located in the bottom-right corner, offering live chat support.

### Detailed Analysis or ### Content Details

* **Logo:** "AT ArbiTool" with the tagline "Professional Arbitrage" below.

* **Headline:** "Did you know that the rate of the same cryptocurrency may vary by up to 50% on two different exchanges?"

* **Description:** "Our tool will show you where and when to buy LOW and sell HIGH."

* **Call-to-Action Buttons:**

* "TELL ME MORE! →" (with a right arrow)

* "TEST IT FOR FREE →" (with a right arrow)

* **Isometric Illustration:** Depicts various elements related to cryptocurrency trading:

* A laptop displaying the ArbiTool logo and a Bitcoin symbol.

* Charts and graphs representing market data.

* Stacks of coins.

* A group of people sitting in a meeting, presumably discussing trading strategies.

* A server rack.

* A tablet displaying charts and graphs.

* **Footer Text:** "Trade our token on:" followed by the Altilly logo.

* **Chat Widget:**

* Text: "We are here! Live chat now."

* "Laissez un message" (French for "Leave a message") with an upward-pointing arrow.

### Key Observations

* The website uses a clean and modern design to appeal to users interested in cryptocurrency trading.

* The headline highlights a significant potential benefit of using the ArbiTool: the ability to profit from price discrepancies between exchanges.

* The call-to-action buttons encourage users to learn more or try the tool for free.

* The isometric illustration visually represents the tool's functionality and target audience.

* The chat widget provides immediate support to website visitors.

### Interpretation

The ArbiTool landing page is designed to attract users interested in cryptocurrency arbitrage. The headline grabs attention by highlighting the potential for significant profits. The description clearly explains the tool's functionality, and the call-to-action buttons encourage users to engage further. The isometric illustration reinforces the tool's focus on cryptocurrency trading and analysis. The presence of a chat widget indicates a commitment to customer support. The page aims to establish ArbiTool as a reliable and effective solution for identifying and exploiting arbitrage opportunities in the cryptocurrency market.

</details>

Figure 5: ArbiTool

At a discretionary level, however, arbitrage opportunities are rarely exploitable due to transfer fees and liquidity issues.

2.1.1 Efficient Market Hypothesis Adaptation to Cryptocurrencies

Fama [Fama, 1970] outlined several conditions for market efficiency and its three forms. Let’s check them for crypto markets.

First, agents should be rational. In crypto, this is unlikely. For example, Dogecoin rose by 14,000% mainly due to memes and social media [Chohan, 2021]:

<details>

<summary>extracted/6391907/images/doge-new.png Details</summary>

### Visual Description

## Time Series Chart: Price Fluctuation Over Time

### Overview

The image is a time series chart displaying price fluctuations over a period from July 2020 to April 2022. The chart shows a significant price increase around April 2021, followed by volatility and a subsequent decline.

### Components/Axes

* **X-axis (Horizontal):** Time, labeled with months and years. Markers are present at:

* Jul 2020

* Oct 2020

* Jan 2021

* Apr 2021

* Jul 2021

* Oct 2021

* Jan 2022

* Apr 2022

* **Y-axis (Vertical):** Price, with numerical markers.

* 0

* 0.1

* 0.2

* 0.3

* 0.4

* 0.5

* 0.6

* 0.7

* **Data Series:** A single line, alternating between green and red, representing the price. Green indicates an increase in price, while red indicates a decrease.

### Detailed Analysis

* **Jul 2020 - Jan 2021:** The price remains relatively stable near 0.

* **Jan 2021 - Apr 2021:** A gradual increase in price begins.

* **Apr 2021 - Jul 2021:** A sharp, rapid increase in price, followed by high volatility with rapid oscillations between green (price increase) and red (price decrease). The price peaks around 0.7.

* **Jul 2021 - Oct 2021:** The price decreases from its peak, with continued volatility.

* **Oct 2021 - Apr 2022:** A gradual decline in price, with decreasing volatility. The price stabilizes around 0.1.

### Key Observations

* The most significant price movement occurs between April 2021 and July 2021.

* The period after the peak shows a clear downward trend.

* Volatility is highest immediately after the price peak.

### Interpretation

The chart illustrates a period of significant price speculation and correction. The initial stable period suggests low interest or activity. The rapid increase in price around April 2021 indicates a surge in demand or speculative investment. The subsequent volatility suggests market uncertainty and price correction, eventually leading to a lower, more stable price point. The data suggests a "pump and dump" scenario, where an asset's price is artificially inflated, followed by a rapid sell-off.

</details>

Figure 6: $\blacktriangle 14,000\%$ DOGE/USD [01/2021-05/2021]

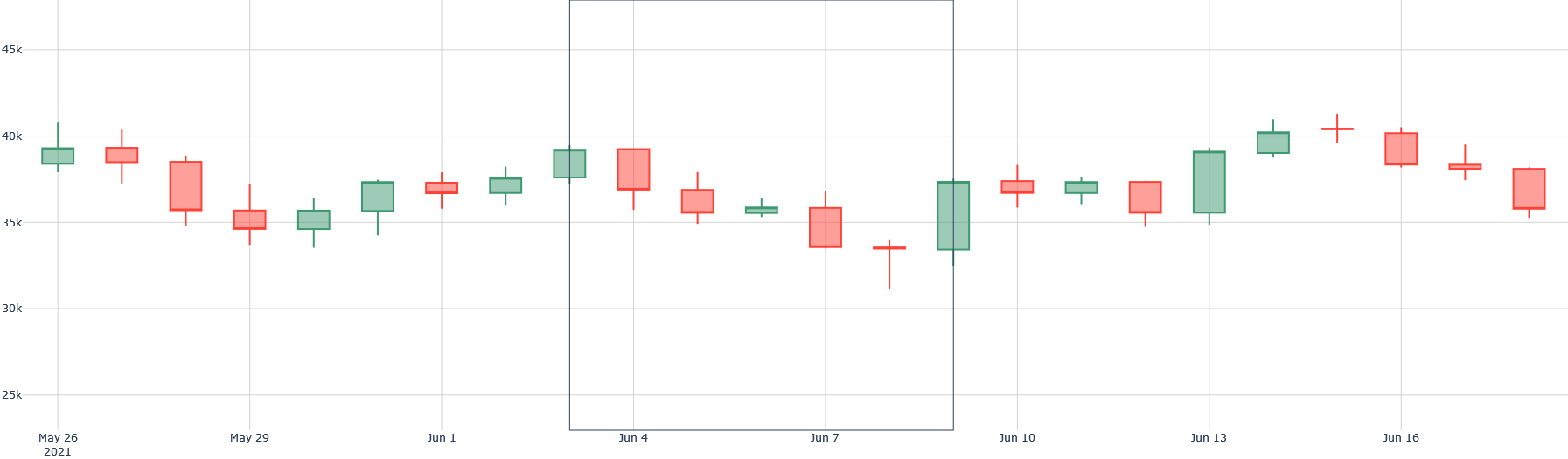

Individuals should not influence the market. Elon Musk, however, can shift prices with a single tweet:

<details>

<summary>extracted/6391907/images/musk1.png Details</summary>

### Visual Description

## Social Media Post: Elon Musk Tweet about Bitcoin

### Overview

The image is a screenshot of a tweet by Elon Musk, using a meme format to comment on Bitcoin. The tweet includes the hashtag "#Bitcoin" followed by a Bitcoin symbol and a broken heart emoji. The meme features a couple sitting on a couch, seemingly in a state of conflict, with overlaid text representing their dialogue.

### Components/Axes

* **Header:**

* **Author:** Elon Musk (@elonmusk)

* **Tweet Content:**

* **Hashtag:** #Bitcoin (followed by Bitcoin symbol and broken heart emoji)

* **Meme Text:**

* Her: I know I said it would be over between us if you quoted another Linkin Park song but I've found someone else.

* Him: So in the end it didn't even matter?

* **Image:** A photo of a man and woman sitting on a couch, looking away from each other with arms crossed.

* **Footer:**

* **Timestamp:** 3:07 AM - 4 juin 2021. Twitter for iPhone

* **Engagement Metrics:**

* 21,1 k Retweets

* 9986 Tweets cités (French: "Quoted Tweets")

* 210,1 k J'aime (French: "Likes")

* **UI Elements:** Twitter icons for reply, retweet, like, and share are present at the bottom.

### Detailed Analysis or ### Content Details

* **Author:** The tweet is attributed to Elon Musk, with the Twitter handle @elonmusk.

* **Hashtag:** The primary topic is Bitcoin, indicated by the "#Bitcoin" hashtag. The Bitcoin symbol and broken heart emoji suggest a negative sentiment or a downturn in Bitcoin's performance.

* **Meme Text:** The meme uses a common relationship breakup scenario, with the "her" character ending the relationship due to the "him" character quoting a Linkin Park song. The "him" character's response is a direct quote from the Linkin Park song "In the End."

* **Image:** The image visually reinforces the meme's theme of conflict and separation. The couple's body language (looking away, arms crossed) suggests disagreement or emotional distance.

* **Timestamp:** The tweet was posted on June 4, 2021, at 3:07 AM.

* **Engagement Metrics:** The tweet has received a significant number of retweets (21,100), quoted tweets (9,986), and likes (210,100).

* **Language:** The tweet is primarily in English, with some French in the engagement metrics ("Tweets cités" and "J'aime").

### Key Observations

* The tweet uses humor and a popular meme format to comment on Bitcoin.

* The broken heart emoji and the meme's theme suggest a negative sentiment towards Bitcoin.

* The high engagement metrics indicate that the tweet resonated with a large audience.

### Interpretation

The tweet is likely a commentary on the volatility or recent performance of Bitcoin. By using the Linkin Park song quote "In the end, it didn't even matter," Musk implies that despite the initial hype or expectations surrounding Bitcoin, its value or impact may have diminished. The broken heart emoji further reinforces this sentiment of disappointment or loss. The tweet's popularity suggests that many users share a similar sentiment regarding Bitcoin. The use of a meme makes the message more accessible and relatable to a wider audience.

</details>

Figure 7: Negative tweet on 04/06/2021

<details>

<summary>extracted/6391907/images/btc-new3.png Details</summary>

### Visual Description

## Candlestick Chart: Price Fluctuations

### Overview

The image presents a candlestick chart illustrating price fluctuations over time. The chart spans from May 26, 2021, to June 16, 2021. Each candlestick represents a trading day, with green candles indicating a price increase and red candles indicating a price decrease. The y-axis represents the price in thousands (k).

### Components/Axes

* **X-axis:** Represents time, with labels indicating specific dates: May 26 2021, May 29, Jun 1, Jun 4, Jun 7, Jun 10, Jun 13, Jun 16.

* **Y-axis:** Represents price, with markers at 25k, 30k, 35k, 40k, and 45k.

* **Candlesticks:** Each candlestick shows the open, close, high, and low prices for a specific day.

* **Green Candlesticks:** Indicate that the closing price was higher than the opening price.

* **Red Candlesticks:** Indicate that the closing price was lower than the opening price.

* **Vertical Rectangle:** A vertical rectangle spans from approximately June 3 to June 9.

### Detailed Analysis

* **May 26, 2021:** Green candlestick, indicating a price increase. The body of the candle is approximately between 38k and 40k.

* **May 29:** Red candlestick, indicating a price decrease. The body of the candle is approximately between 35k and 39k.

* **Jun 1:** Green candlestick, indicating a price increase. The body of the candle is approximately between 36k and 37k.

* **Jun 4:** Red candlestick, indicating a price decrease. The body of the candle is approximately between 36k and 39k.

* **Jun 7:** Red candlestick, indicating a price decrease. The body of the candle is approximately between 34k and 36k.

* **Jun 10:** Green candlestick, indicating a price increase. The body of the candle is approximately between 34k and 37k.

* **Jun 13:** Green candlestick, indicating a price increase. The body of the candle is approximately between 37k and 39k.

* **Jun 16:** Red candlestick, indicating a price decrease. The body of the candle is approximately between 36k and 40k.

### Key Observations

* The price fluctuates between approximately 33k and 41k during the observed period.

* There are periods of both increasing and decreasing prices, as indicated by the alternating green and red candlesticks.

* The vertical rectangle highlights a period of price volatility or specific interest between June 3 and June 9.

### Interpretation

The candlestick chart provides a visual representation of price movements over a short period. The alternating green and red candlesticks suggest a market with frequent changes in sentiment. The vertical rectangle could indicate a period of increased trading volume, news events, or other factors that influenced price fluctuations. The chart does not provide information about the specific asset being tracked, but it offers insights into its price behavior during the specified timeframe.

</details>

Figure 8: Observed correlation: $\blacktriangledown 15\%$ BTC/USD [04/06/2021-08/06/2021]

No information asymmetry should exist. Yet, insider knowledge (e.g., hacks) creates advantages [Biais et al., 2020].

Information should be free. For crypto, public data is widely available, though high-frequency trading data is costly [Grossman and Stiglitz, 1976].

Taxes should be low. Given international diversity, this varies.

Regarding efficiency forms:

Strong form: all public and private info is priced. However, events like Binance’s launch in 2017 or the Bitconnect scandal in 2018 show that insiders could have benefited:

<details>

<summary>extracted/6391907/images/btc-new4.png Details</summary>

### Visual Description

## Candlestick Chart: Stock Price Trend (Jun-Oct 2017)

### Overview

The image is a candlestick chart showing the price fluctuations of a stock or asset over time, from June 11, 2017, to October 1, 2017. The chart uses green and red candlesticks to represent price increases and decreases, respectively.

### Components/Axes

* **X-axis (Time):** Labeled with dates: Jun 11 2017, Jun 25, Jul 9, Jul 23, Aug 6, Aug 20, Sep 3, Sep 17, Oct 1.

* **Y-axis (Price):** Labeled with values: 1000, 2000, 3000, 4000, 5000, 6000, 7000.

* **Candlesticks:**

* **Green:** Indicates a price increase (closing price higher than opening price).

* **Red:** Indicates a price decrease (closing price lower than opening price).

* The body of the candlestick represents the range between the opening and closing prices.

* The "wicks" or "shadows" extending from the body represent the high and low prices for that period.

### Detailed Analysis

* **Jun 11 - Jun 25:** The price fluctuates between approximately 2500 and 3000, with a mix of green and red candlesticks, indicating a period of relative stability.

* **Jun 25 - Jul 9:** A slight downward trend is visible, with the price decreasing from around 2700 to approximately 2400.

* **Jul 9 - Aug 6:** A clear upward trend begins, with the price increasing from approximately 2000 to around 3500.

* **Aug 6 - Aug 20:** The upward trend continues, with the price reaching approximately 4500.

* **Aug 20 - Sep 3:** The price fluctuates significantly, reaching a high of approximately 4800 before dropping to around 3800.

* **Sep 3 - Sep 17:** A downward trend is observed, with the price decreasing from approximately 4800 to around 3200.

* **Sep 17 - Oct 1:** A strong upward trend resumes, with the price increasing from approximately 3800 to around 5800.

### Key Observations

* The chart shows periods of both upward and downward trends, as well as periods of relative stability.

* The most significant price increase occurs between Sep 17 and Oct 1.

* The most significant price decrease occurs between Aug 20 and Sep 17.

### Interpretation

The candlestick chart provides a visual representation of the price movements of an asset over time. The trends suggest periods of buying and selling pressure, with the overall trend being upward from July to October. The fluctuations could be due to various market factors, such as news events, economic data, or investor sentiment. The strong upward trend at the end of the period suggests increasing investor confidence or positive developments related to the asset.

</details>

Figure 9: $\blacktriangle 150\%$ BTC/USD [13/06/2017-01/09/2017]

<details>

<summary>extracted/6391907/images/btc-new5.png Details</summary>

### Visual Description

## Candlestick Chart: Stock Price Fluctuation

### Overview

The image presents a candlestick chart illustrating price fluctuations over time. The chart spans from December 2017 to March 2018. The y-axis represents price in thousands (k), ranging from 4k to 22k. The x-axis represents time, marked with dates. The chart uses green and red candlesticks to indicate price increases and decreases, respectively. A vertical grey box highlights a specific time period.

### Components/Axes

* **Y-Axis:** Price (in thousands), ranging from 4k to 22k, with increments of 2k.

* **X-Axis:** Time, labeled with dates: Dec 10 2017, Dec 24, Jan 7 2018, Jan 21, Feb 4, Feb 18, Mar 4.

* **Candlesticks:** Green candlesticks indicate price increases, while red candlesticks indicate price decreases. Each candlestick represents the open, close, high, and low prices for a specific period.

* **Grey Box:** A vertical grey box highlights the period between Jan 7 2018 and Jan 21.

### Detailed Analysis

* **Dec 10 2017 to Dec 24:** The price generally increases from approximately 11k to 20k, with some fluctuations. There are both green and red candlesticks, but the overall trend is upward.

* **Dec 24 to Jan 7 2018:** The price decreases from approximately 20k to 14k. The candlesticks are predominantly red, indicating a downward trend.

* **Jan 7 2018 to Jan 21:** The price continues to decrease, reaching approximately 11k. The candlesticks are mostly red.

* **Jan 21 to Feb 4:** The price decreases further, reaching a low of approximately 7k. The candlesticks are predominantly red.

* **Feb 4 to Feb 18:** The price increases from approximately 7k to 10k. The candlesticks are mostly green, indicating an upward trend.

* **Feb 18 to Mar 4:** The price fluctuates around 10k, with both green and red candlesticks. The overall trend is relatively stable.

### Key Observations

* The period from Dec 10 2017 to Dec 24 shows a significant price increase.

* The period from Dec 24 to Feb 4 shows a significant price decrease.

* The price appears to stabilize around 10k from Feb 18 to Mar 4.

* The grey box highlights a period of price decline.

### Interpretation

The candlestick chart illustrates the volatility of the price over time. The initial increase from Dec 2017 is followed by a significant decline into early February 2018. The price then shows signs of stabilization. The grey box highlights a period of significant price decline, suggesting a period of market correction or negative news. The chart provides a visual representation of market trends and can be used to identify potential buying or selling opportunities.

</details>

Figure 10: $\blacktriangledown 15\%$ BTC/USD [16/01/2018-17/01/2018]

Semi-strong form: all public info is priced. The crypto market reacts quickly to news, as seen with Coinbase’s NASDAQ listing:

<details>

<summary>extracted/6391907/images/btc-new6.png Details</summary>

### Visual Description

## Candlestick Chart: Price Fluctuations Over Time

### Overview

The image presents a candlestick chart illustrating price fluctuations over time. The chart spans from approximately March 14, 2021, to May 23, 2021. Each candlestick represents a trading day, with green candles indicating a price increase and red candles indicating a price decrease. The y-axis represents the price in thousands (k).

### Components/Axes

* **Y-Axis (Price):** The vertical axis represents the price, with markers at 50k, 55k, 60k, and 65k.

* **X-Axis (Time):** The horizontal axis represents time, with markers at March 14, 2021, March 28, April 11, April 25, May 9, and May 23.

* **Candlesticks:** Each candlestick shows the open, close, high, and low prices for a specific day.

* **Green Candlesticks:** Indicate that the closing price was higher than the opening price.

* **Red Candlesticks:** Indicate that the closing price was lower than the opening price.

* **Gridlines:** Light gray gridlines are present, aiding in the visual estimation of price levels.

### Detailed Analysis

* **March 14, 2021:** The price starts around 52k.

* **March 14 - March 28:** The price fluctuates, with a mix of green and red candlesticks, generally trending upwards to approximately 57k.

* **March 28 - April 11:** The price continues to fluctuate, with a mix of green and red candlesticks, generally trending upwards to approximately 64k.

* **April 11 - April 25:** The price experiences a significant drop, with predominantly red candlesticks, falling to approximately 49k.

* **April 25 - May 9:** The price recovers somewhat, with a mix of green and red candlesticks, rising to approximately 58k.

* **May 9 - May 23:** The price declines sharply again, with predominantly red candlesticks, falling to approximately 47k.

### Key Observations

* **Volatility:** The price exhibits significant volatility throughout the period, with alternating periods of increase and decrease.

* **Peak:** The highest price point is reached around April 11, at approximately 64k.

* **Trough:** The lowest price point is reached around May 23, at approximately 47k.

* **Sharp Decline:** There are two notable sharp declines: one between April 11 and April 25, and another between May 9 and May 23.

### Interpretation

The candlestick chart illustrates the price dynamics of an asset over a two-month period. The alternating green and red candlesticks indicate daily price fluctuations, while the overall trend reveals periods of growth and decline. The sharp declines suggest potential market corrections or negative news events impacting the asset's value. The volatility observed throughout the period indicates a degree of risk associated with this asset. The chart suggests that the asset experienced a significant correction in late April and mid-May, after reaching a peak in early April.

</details>

Figure 11: $\blacktriangledown 22\%$ BTC/USD [14/04/2021-25/04/2021]

The day before its IPO, BTC/USD increased by almost 7%, before losing more than 20% ten days later. The weak form assumes that all historical price information is already reflected in the current price. This form challenges technical analysis, which specializes precisely in analyzing past returns. These analyses are widely shared on social media, due to their ease of implementation, and attract a (too?) proselytizing community. The idea is to use indicators mainly based on past fluctuations to make future predictions. Among the usual indicators (according to the TA-Lib library, considered a reference) are: RSI (Relative Strength Index), SMA (Simple Moving Average), BBANDS (Bollinger Bands). Let us check, for example, whether a "mean-reversion" strategy would be more effective than a simple "hold" (buy-sell only once) and more effective than a random strategy by backtesting these strategies on 2021. If not, we could conjecture that, over the entire year of 2021, it was useless to use a "mean-reversion" strategy (which assumes that when the current price is too "far" from the moving average (SMA), the price will return to its "mean")). This may also give us an indication about the market efficiency form.

We will base our analysis on a set $\Omega$ of crypto-assets. For each element in $\Omega$ , we will test three strategies: mean-reversion, hold, and random. We assume short-selling is allowed. Let $P_{t}$ be the price at time $t$ , $M_{t}(n)$ the moving average at time $t$ with a window of $n$ days, $\omega_{i}$ the $i^{th}$ element of $\Omega$ , and $r∈[0,100]$ a percentage around $M_{t}(n)$ indicating the threshold at which we open/close a position. The mean-reversion strategy will be constructed as follows: if $P_{t}>M_{t}(n)+(\frac{M_{t}(n)× r}{100})$ , then sell $\omega_{i}$ at price $P_{t}$ ; if $P_{t}<M_{t}(n)-(\frac{M_{t}(n)× r}{100})$ , then buy $\omega_{i}$ at price $P_{t}$ , with $t$ ranging from [01/01/2021, 31/12/2021].

The hold strategy will be constructed as follows: if $t=01/01/2021$ , then buy $\omega_{i}$ at price $P_{t}$ ; if $t=31/12/2021$ , then sell $\omega_{i}$ at price $P_{t}$ .

The random strategy will be constructed as follows: generate a signal $S∈[\text{buy, sell, hold}]$ with $P(S=\text{buy})=P(S=\text{sell})=P(S=\text{hold})=\frac{1}{3}$ . For each $\omega_{i}$ and for each $t$ , if $S=\text{"buy"}$ we buy $\omega_{i}$ at price $P_{t}$ , if $S=\text{"sell"}$ we sell $\omega_{i}$ at price $P_{t}$ , if $S=\text{"hold"}$ we do nothing.

Thus, we create a Python function isSMABetter( $\Omega,n,r$ ) that takes as parameters $\Omega$ (the set of crypto-assets), $r$ (the percentage for the SMA thresholds), and $n$ (the window size in days for the SMA), and returns True if the average SMA returns of $\omega_{i}$ are greater than the average returns of the hold strategy and (strictly) the random strategy in at least 50% of the cases, and False otherwise.

We only consider daily returns. Indeed, how could we backtest a strategy that only opens positions? We thus place ourselves in a short-term trading scale for each trade, which is consistent with the chartist approach (otherwise, we would prefer a passive investment strategy that requires almost no analysis).

The results of isSMABetter( $\Omega,n,r$ ), whose code is in Appendix B, are as follows:

| 116 | 1179 | -484 | -4 | 50 | 20 | 0.00 | False |

| --- | --- | --- | --- | --- | --- | --- | --- |

Table 2: Results of isSMABetter( $\Omega,n,r$ )

It appears that in 2021, among the 116 crypto-assets tested, it was more optimal to have a passive strategy or, at worst, a random strategy, rather than using the moving average in an attempt to generate profits with a day-trading approach (speculation aiming to make a profit within the same day of a market order execution), since the average return obtained with the SMA strategy was the lowest among the three (-484%), and strictly no crypto-asset (0%) showed any interest in being traded with an SMA strategy.

We can conjecture that the cryptocurrency market efficiency form is at least weak, and possibly semi-strong, depending on the crypto-assets and periods, but hardly strong.

2.1.2 Random Walk and Martingale

In almost all the literature ([Lardic and Mignon, 2006], [Jovanovic, 2009] …), a random walk is modeled by two elements: the previous observation and white noise. The literature explains that a price can be modeled as: $P_{t+1}=P_{t}+\varepsilon_{t+1}$ , with $\varepsilon=\{\varepsilon_{t},t∈ N\}$ being white noise. This implies that the best (and only) way to predict the price of an asset is by using its current price.

We will perform a Dickey-Fuller test [Dickey and Fuller, 1979] on each element of a set of assets $\Omega$ with a significance level of $\alpha=5\%$ . We define a Python function getRandomPerc( $\Omega$ ) that takes as input a set of crypto-assets $\Omega$ and returns the percentage of assets in that set that appear to follow a random walk, that is, for which we do not reject the null hypothesis "the time series is non-stationary". The result of getRandomPerc( $\Omega$ ), whose code is provided in Appendix F, returns 69 %. It seems that more than half of the cryptocurrencies follow a random walk.

There is often confusion between efficiency and random walk. Indeed, when reading the Wikipedia page on the efficient market hypothesis, one might think that an efficient market necessarily implies prices following a random walk. However, this is false. The market is not necessarily inefficient if prices do not follow a random walk because, as [Lardic and Mignon, 2006] states, "It suffices, for example, that the hypothesis of risk neutrality is not satisfied, or that individuals’ utility functions are not separable and additive [LeRoy, 1982], meaning that it is impossible to separate consumption and investment decisions."

Many studies show that cryptocurrencies (most studies focus on Bitcoin) do not follow a random walk ([Palamalai et al., 2021], [Aggarwal, 2019] …). However, these studies mainly rely on the very restrictive assumption of autocorrelation, and conclude that the Bitcoin market is not efficient. Samuelson [Samuelson, 2016] already addressed this problem in his time and proposed a modification to the random walk hypothesis: the martingale model.

This model is less restrictive than the random walk model because it imposes no condition on the autocorrelation of residuals. Very similar to the previous model, a price process $P_{t}$ follows a martingale if: $E[P_{t+1}|I_{t}]=P_{t}$ , where $P_{t}$ is the price at time $t$ and $I_{t}$ is the information set at time $t$ . Thus, under the martingale model, the current price is the sole (and best) predictor of the next price, even if there are successive dependencies in returns.

As previously noted, an analysis of most cryptocurrencies (the most widely used) shows that the returns of more than half of the assets seem to follow a random walk. With the martingale model, one might be tempted to assert that the crypto market is efficient.

However, many studies have investigated the relationship between Bitcoin and the martingale model ([Zargar and Kumar, 2019], [Nadarajah and Chu, 2017] …) and conclude that the Bitcoin market is not efficient, mainly due to endogenous factors of an emerging and immature market, and the absence of traders relying on fundamental value.

It is difficult to extend this conclusion to the entire cryptocurrency market. However, we know that a study showing market inefficiency between 2012 and 2015 is not highly relevant for 2022, as much has happened since then (especially for Bitcoin).

Thus, we highlight the application of Lo’s adaptive market hypothesis [Lo, 2004] to Bitcoin through a study [Khuntia and Pattanayak, 2018], which explains that efficiency improves over time. This study particularly well summarizes the evolution of crypto market returns: episodes of efficiency and inefficiency, creating opportunities for arbitrage and above-average returns, but an impossibility to predict these opportunities systematically or mathematically.

2.1.3 Cryptocurrencies and Fundamental Value

As explained by [Delcey et al., 2017], there are two definitions of an efficient market. Fama’s definition implies that the randomness of a price is explained by the fact that prices converge toward the fundamental value. Samuelson’s definition implies that unpredictable price variations are simply the result of competition among investors, regardless of fundamental value. This raises the following question: What is a fundamental value for a cryptocurrency?

According to [Biais et al., 2020], the fundamental value of Bitcoin (and by extension most other cryptocurrencies, as they hardly differ in their characteristics) lies in its stream of net transactional benefits, which depend on its future prices. These transactional benefits may, for instance, represent the ability to exchange money in an unstable economic and financial system (such as in Venezuela or Zimbabwe), or when exchanges are blocked or heavily taxed.

To determine the net value, [Biais et al., 2020] consider various costs: limited convertibility, transaction fees from brokers, mining costs, and crash risk. They thus provide a definition of Bitcoin’s fundamental value (and technically of other cryptocurrencies) and answer the question of whether a cryptocurrency can have a fundamental value.

Obviously, this value differs depending on the cryptocurrency. For instance, if there is a strong demand for privacy in transactions, Monero (XMR) would dominate in volume, since it uses a private blockchain by default (making transactions untraceable, unlike Bitcoin where the blockchain is public and all transactions are identifiable).

However, the very idea that Bitcoin has a fundamental value is debated both in the media and academic literature. According to [Yermack, 2013], cryptocurrencies have no fundamental value because, if they did, there would be no incentive to mine cryptocurrency. According to [Hanley, 2013], Bitcoin’s value merely floats relative to other currencies as a market estimate without any fundamental value to support it. [Woo et al., 2013] suggests Bitcoin may have a certain fair value because of its features similar to fiat currencies (means of exchange and store of value), but without any other underlying basis.

[Hayes, 2015] links the importance of Bitcoin’s mining network to the dependency of altcoin holders on Bitcoin, given that most altcoins must be exchanged into Bitcoin before being converted into fiat currency for real-world use. Furthermore, [Garcia et al., 2014] highlights the importance of mining production costs in the fundamental value of cryptocurrencies, as it provides a kind of “floor value”.

Cryptocurrencies are often criticized for being "backed by nothing", a misconception regarding the role of money in an economy. For example, according to the U.S. Federal Reserve, “ Federal Reserve notes are not redeemable in gold, silver, or any other commodity. Federal Reserve notes have not been redeemable in gold since January 30, 1934, when the Congress amended Section 16 of the Federal Reserve Act to read: "The said [Federal Reserve] notes shall be obligations of the United States….They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank." ”

Beyond the purely economic definition of value (utility and scarcity), for which Bitcoin qualifies (its utility lying in being an alternative to the centralized financial system, and its scarcity from the 21 million unit limit and diminishing accessibility over time), there is also a subjective characteristic to this value.

We highlight two relevant elements: network value and safe-haven value. According to Metcalfe’s law [Metcalfe, 1995], although nuanced [Odlyzko and Tilly, 2005], the value of a network is proportional to the square of the number of its users: a single fax machine is useless, but the value of each fax increases with the total number of machines in the network. One could thus infer a similar characteristic for cryptocurrencies.

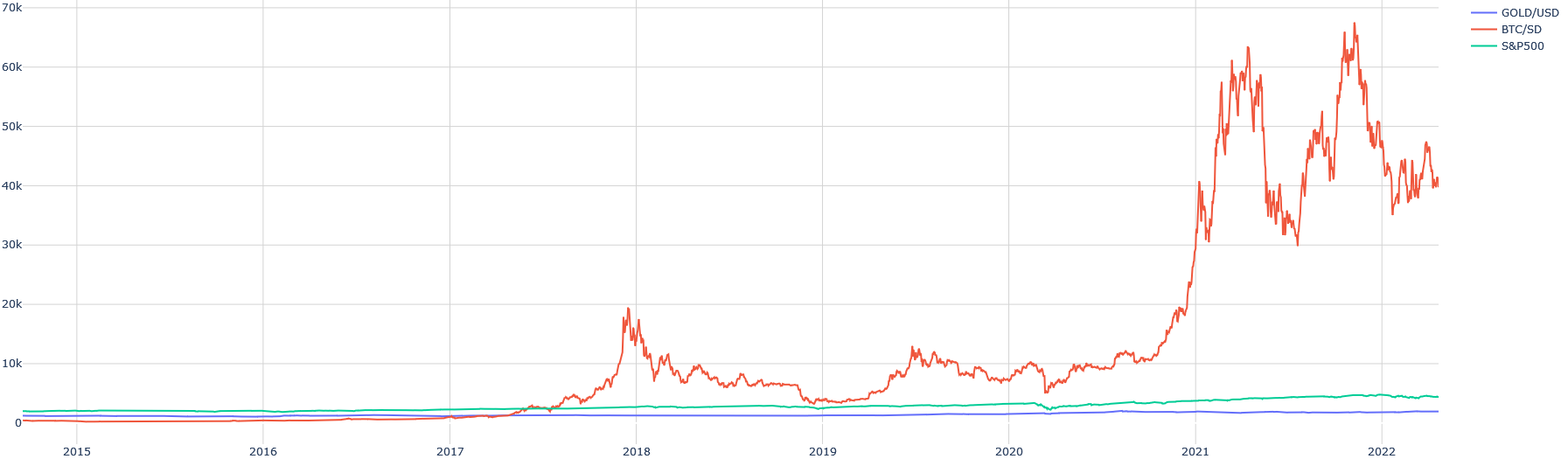

According to [Baur and McDermott, 2010], a safe-haven asset can be defined as one that is negatively correlated with equities during crises. Gold is often a reference point. Let us verify this. We cannot directly compare superimposed charts due to vastly different magnitudes:

<details>

<summary>extracted/6391907/images/cor1.png Details</summary>

### Visual Description

## Line Chart: GOLD/USD, BTC/SD, and S&P500 Performance (2015-2022)

### Overview

The image is a line chart comparing the performance of GOLD/USD, BTC/SD (Bitcoin), and the S&P500 index from 2015 to 2022. The chart displays the price trends of these three assets over time, with the y-axis representing price in thousands (k) and the x-axis representing the year.

### Components/Axes

* **X-axis:** Represents time, labeled with years from 2015 to 2022.

* **Y-axis:** Represents price in thousands (k), with markers at 0, 10k, 20k, 30k, 40k, 50k, 60k, and 70k.

* **Legend (Top-Right):**

* Blue line: GOLD/USD

* Red line: BTC/SD

* Green line: S&P500

### Detailed Analysis

* **GOLD/USD (Blue Line):**

* Trend: Relatively stable with a slight upward trend.

* Approximate Values: Starts around 1.1k in 2015 and ends around 1.8k in 2022.

* **BTC/SD (Red Line):**

* Trend: Highly volatile with significant price increases, especially after 2020.

* Approximate Values: Starts around 0.3k in 2015, experiences a spike to approximately 18k in early 2018, then fluctuates between 6k and 12k until 2020. After 2020, it rises dramatically, peaking at approximately 65k in late 2021, before declining to around 38k in 2022.

* **S&P500 (Green Line):**

* Trend: Steady upward trend.

* Approximate Values: Starts around 2.1k in 2015 and ends around 4.0k in 2022.

### Key Observations

* BTC/SD shows the most significant price fluctuations and overall growth compared to GOLD/USD and S&P500.

* GOLD/USD exhibits the least volatility and the smallest overall growth.

* S&P500 demonstrates a consistent, moderate growth rate.

* The period after 2020 shows a significant divergence in performance, with BTC/SD experiencing exponential growth and subsequent decline.

### Interpretation

The chart illustrates the differing investment profiles of gold, Bitcoin, and the S&P500. Bitcoin's high volatility and potential for high returns are evident, while gold offers stability and lower returns. The S&P500 provides a balance between risk and return, with steady growth over the period. The dramatic rise and fall of Bitcoin after 2020 highlights the speculative nature of cryptocurrency investments. The data suggests that Bitcoin's performance is largely independent of the other two assets, while gold and the S&P500 show a more consistent, albeit less dramatic, growth pattern.

</details>

Figure 12: Correlation between BTC/USD, GOLD/USD, and S&P500

Thus, we will separately analyze the correlation between S&P500 crashes and BTC/USD prices:

<details>

<summary>extracted/6391907/images/sp.png Details</summary>

### Visual Description

## Line Chart: Time Series Data

### Overview

The image is a line chart displaying a time series of data from 2015 to 2022. The y-axis represents a numerical value ranging from approximately 2000 to 4500, while the x-axis represents time in years. The single blue line shows the trend of the data over time.

### Components/Axes

* **X-axis:** Years from 2015 to 2022.

* **Y-axis:** Numerical values ranging from 2000 to 4500, with increments of 500.

* **Data Series:** A single blue line representing the data.

### Detailed Analysis

* **2015:** The blue line starts at approximately 2000.

* **2016:** The line fluctuates around 2000, with a slight dip below 2000.

* **2017:** The line shows an upward trend, reaching approximately 2500.

* **2018:** The upward trend continues, reaching approximately 2800.

* **2019:** The line fluctuates around 3000, with a dip towards the end of the year.

* **2020:** A significant drop occurs in early 2020, reaching a low of approximately 2250, followed by a sharp recovery.

* **2021:** The line shows a strong upward trend, reaching approximately 4250.

* **2022:** The line fluctuates around 4500, with a slight downward trend towards the end of the year.

### Key Observations

* The data shows a general upward trend from 2015 to 2022, with a significant drop in early 2020.

* The most substantial growth occurs between 2020 and 2021.

* The data fluctuates significantly in 2022.

### Interpretation

The line chart likely represents a stock market index or similar financial data. The upward trend suggests growth over the period, while the drop in 2020 likely corresponds to a significant economic event, such as the COVID-19 pandemic. The fluctuations in 2022 could indicate market volatility or uncertainty.

</details>

Figure 13: S&P500 over the period available with BTC/USD

We notice graphical correlations during several crash periods:

- Early 2018

- Late 2019

- Early 2020

- Early 2022

These correlations are weaker, or even negative, with gold:

<details>

<summary>extracted/6391907/images/gold.png Details</summary>

### Visual Description

## Line Chart: Time Series Data

### Overview

The image is a line chart displaying time series data. The x-axis represents time, spanning from 2015 to 2022. The y-axis represents a numerical value, ranging from 1000 to 2000. A single blue line plots the data points over time, showing fluctuations and trends.

### Components/Axes

* **X-axis:**

* Label: Years

* Scale: 2015, 2016, 2017, 2018, 2019, 2020, 2021, 2022

* **Y-axis:**

* Label: Numerical Value (unspecified units)

* Scale: 1000, 1200, 1400, 1600, 1800, 2000

* **Data Series:**

* Color: Blue

* Trend: Fluctuating with an overall upward trend, especially pronounced after 2019.

### Detailed Analysis

* **2015:** Starts around 1200, fluctuates down to approximately 1100, then back up.

* **2016:** Begins around 1200, rises to approximately 1350, then declines.

* **2017:** Starts around 1250, fluctuates around 1300.

* **2018:** Remains relatively stable, fluctuating around 1300.

* **2019:** Starts around 1300, ends around 1400.

* **2020:** Shows a significant upward trend, rising from approximately 1400 to 1800.

* **2021:** Peaks around 1950-2000, then declines to approximately 1700-1800.

* **2022:** Fluctuates around 1800-1900, ending near 1900.

### Key Observations

* The data shows a period of relative stability between 2017 and 2019.

* A significant increase occurs in 2020.

* The highest point is reached in 2021, followed by a decline and stabilization.

### Interpretation

The line chart illustrates the trend of a numerical value over time. The period from 2015 to 2019 shows moderate fluctuations, while 2020 marks a significant turning point with a substantial increase. The peak in 2021 is followed by a correction, and the value stabilizes at a higher level in 2022 compared to the pre-2020 period. This suggests a potential shift in the underlying factors influencing the numerical value around 2020.

</details>

Figure 14: GOLD/USD over the period available with BTC/USD

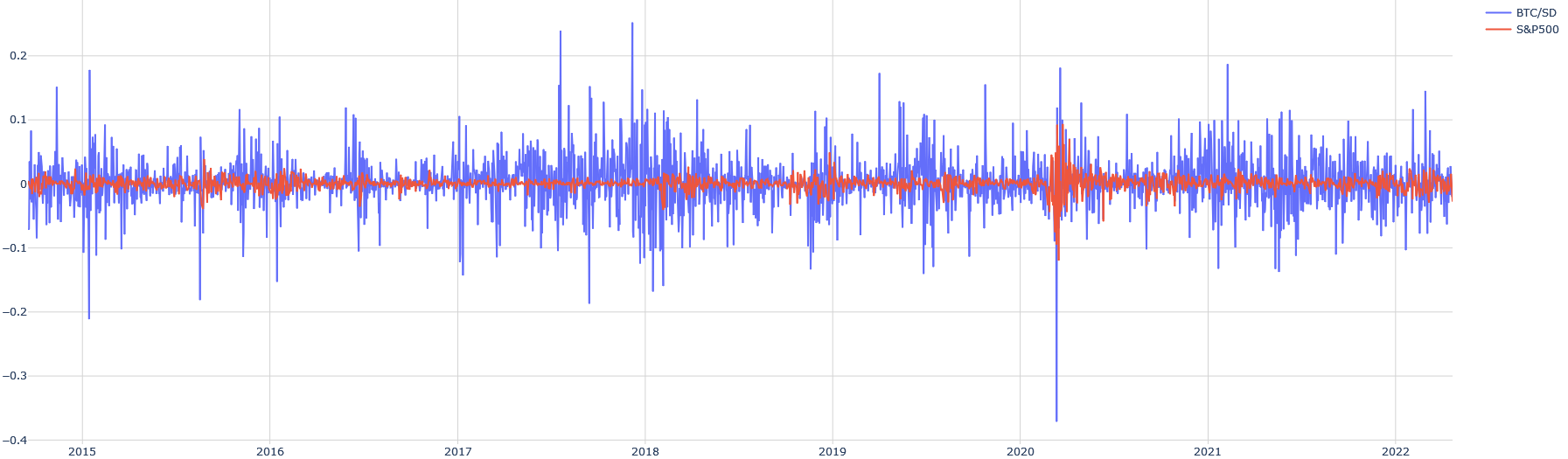

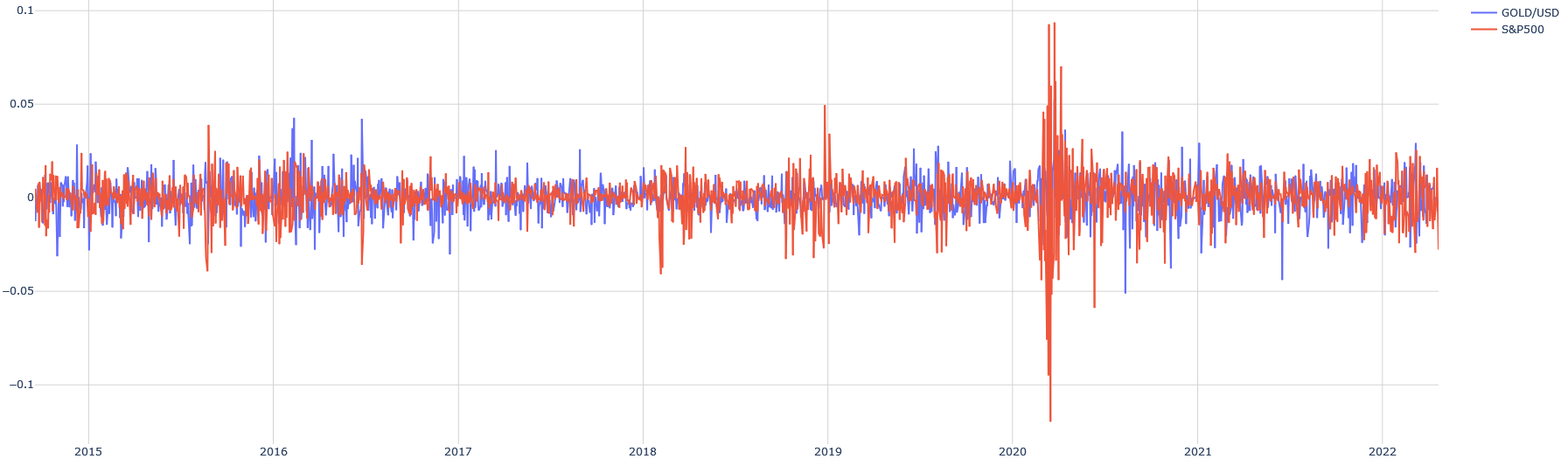

Let us graphically check the correlation of daily returns:

<details>

<summary>extracted/6391907/images/cor-btc-sp.png Details</summary>

### Visual Description

## Line Chart: BTC/SD vs. S&P500

### Overview

The image is a line chart comparing the fluctuations of BTC/SD (Bitcoin Standard Deviation) and S&P500 over time, from 2015 to 2022. The chart displays the volatility of BTC/SD relative to the S&P500, with BTC/SD showing significantly higher fluctuations.

### Components/Axes

* **X-axis:** Represents time, labeled with years from 2015 to 2022.

* **Y-axis:** Represents the value, ranging from -0.4 to 0.2, with increments of 0.1.

* **Legend (Top-Right):**

* Blue line: BTC/SD

* Red line: S&P500

### Detailed Analysis

* **BTC/SD (Blue Line):** The BTC/SD line shows high volatility with frequent and large swings both above and below the zero line.

* From 2015 to early 2018, the fluctuations are generally within the range of -0.1 to 0.1, with occasional spikes.

* In 2018, the volatility increases, with peaks reaching above 0.2 and troughs going below -0.2.

* A significant drop occurs around 2020, reaching approximately -0.4.

* After 2020, the volatility remains high, but the range of fluctuations seems to narrow slightly compared to 2018.

* **S&P500 (Red Line):** The S&P500 line shows relatively low volatility, staying close to the zero line throughout the entire period.

* The line fluctuates slightly around zero, with occasional deviations.

* Around 2020, there is a noticeable dip, but it is much less severe than the drop observed in the BTC/SD line.

### Key Observations

* **Volatility:** BTC/SD is significantly more volatile than the S&P500.

* **Correlation:** While both lines show some dips around 2020, the magnitude of the changes is vastly different, suggesting a weak correlation.

* **Range:** The S&P500 remains within a narrow range close to zero, while BTC/SD experiences much wider swings.

### Interpretation

The chart illustrates the higher risk and volatility associated with Bitcoin compared to the S&P500. The S&P500, representing a broader market index, exhibits more stability. The large fluctuations in BTC/SD suggest that it is more susceptible to market events and investor sentiment. The relatively stable S&P500 indicates a more diversified and less volatile investment. The data suggests that while both assets experienced a dip around 2020, the impact on Bitcoin was far more pronounced, highlighting its higher risk profile.

</details>

Figure 15: Correlation between BTC/USD and S&P500 (daily returns)

<details>

<summary>extracted/6391907/images/cor-gold-sp.png Details</summary>

### Visual Description

## Time Series Chart: GOLD/USD vs. S&P500

### Overview

The image is a time series chart comparing the fluctuations of GOLD/USD and S&P500 from 2015 to 2022. The chart displays the daily changes of the two assets over time.

### Components/Axes

* **X-axis:** Time, labeled with years from 2015 to 2022.

* **Y-axis:** Values ranging from -0.1 to 0.1, with increments of 0.05.

* **Legend (Top-Right):**

* Blue line: GOLD/USD

* Red line: S&P500

### Detailed Analysis

* **GOLD/USD (Blue Line):**

* General Trend: Fluctuates around 0, showing volatility over time.

* 2015-2019: Relatively stable fluctuations between approximately -0.02 and 0.02.

* 2020: Experiences a significant drop to approximately -0.07, followed by a sharp recovery.

* 2021-2022: Continues to fluctuate, with peaks and valleys generally within the -0.04 to 0.04 range.

* **S&P500 (Red Line):**

* General Trend: Similar to GOLD/USD, fluctuates around 0, indicating volatility.

* 2015-2019: Fluctuations are generally between -0.02 and 0.02.

* 2020: Shows a dramatic drop to approximately -0.1, followed by a rapid spike to around 0.09.

* 2021-2022: Continues to fluctuate, with peaks and valleys generally within the -0.03 to 0.03 range.

### Key Observations

* Both GOLD/USD and S&P500 exhibit significant volatility, particularly around 2020.

* The S&P500 shows a more pronounced spike in volatility in 2020 compared to GOLD/USD.

* Both assets generally fluctuate within a narrow range, but experience occasional extreme deviations.

### Interpretation

The chart illustrates the daily changes of GOLD/USD and S&P500 over a seven-year period. The data suggests that both assets experienced increased volatility around 2020, likely due to global events such as the COVID-19 pandemic. The S&P500 appears to have been more significantly impacted by these events, as evidenced by the larger spike in volatility compared to GOLD/USD. The fluctuations in both assets indicate the dynamic nature of financial markets and the potential for both gains and losses. The data does not provide information about the underlying causes of the fluctuations, but it highlights the importance of monitoring market trends and managing risk.

</details>

Figure 16: Correlation between GOLD/USD and S&P500 (daily returns)

A numerical analysis of the correlation of daily returns over the entire period shows 16% for Bitcoin with the S&P500 and 5% for gold with the S&P500. Bitcoin does not appear to be a better safe-haven asset than gold, which is confirmed by other studies ([Smales, 2019], [Bouri et al., 2017]).

2.2 From Louis Bachelier to Contemporary Models

Eugène Fama is not the inventor of the idea of a random market. We can trace it back to 1863, when Jules Regnault [Regnault, 1863] proposed a model of randomly volatile markets. Then, in 1900, Bachelier [Bachelier, 1900] formalized it. It was only from the 1930s that the random aspect of the market began to be considered, notably in the United States with the emergence of econometrics, and then, from the 1960s, financial economics in the United States started to connect the model to economic theory, giving rise to the theory of informational efficiency of financial markets. However, this theory, although constituting the foundation of the random walk model, would never achieve unanimous acceptance. In this subsection, we will present the theoretical models that have explained the variations of financial assets since 1900, from Louis Bachelier’s theory of speculation to the present day.

2.2.1 Modeling of Traditional Finance

It is important to understand that the cryptocurrency market is not disconnected from traditional financial markets in its creation.

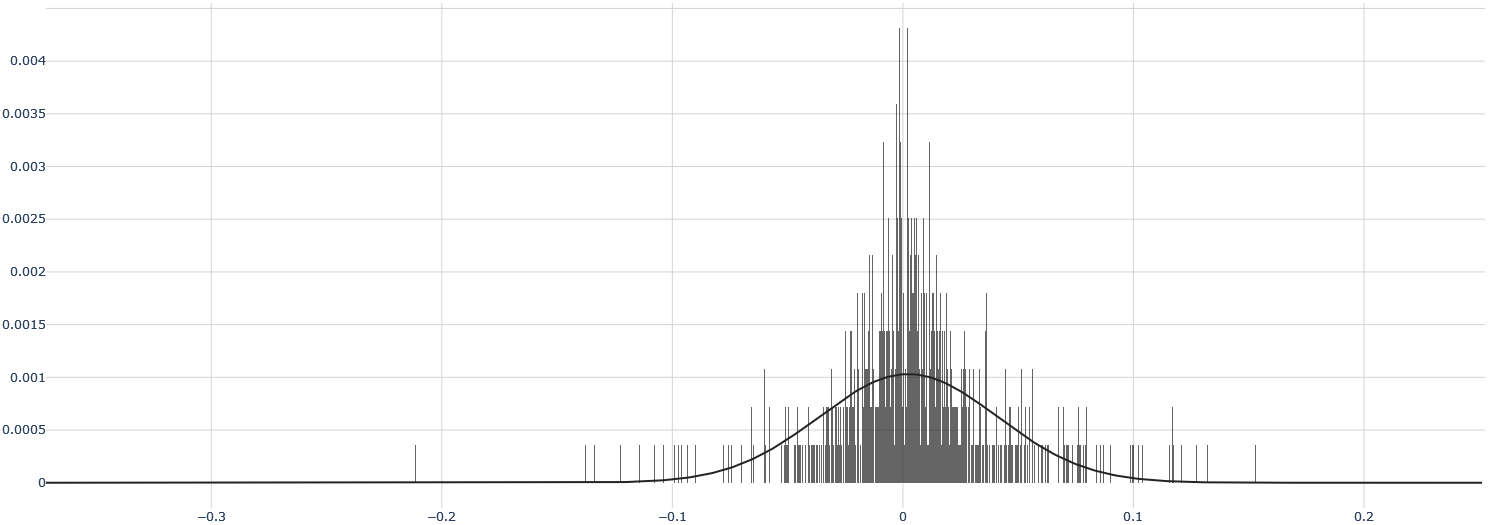

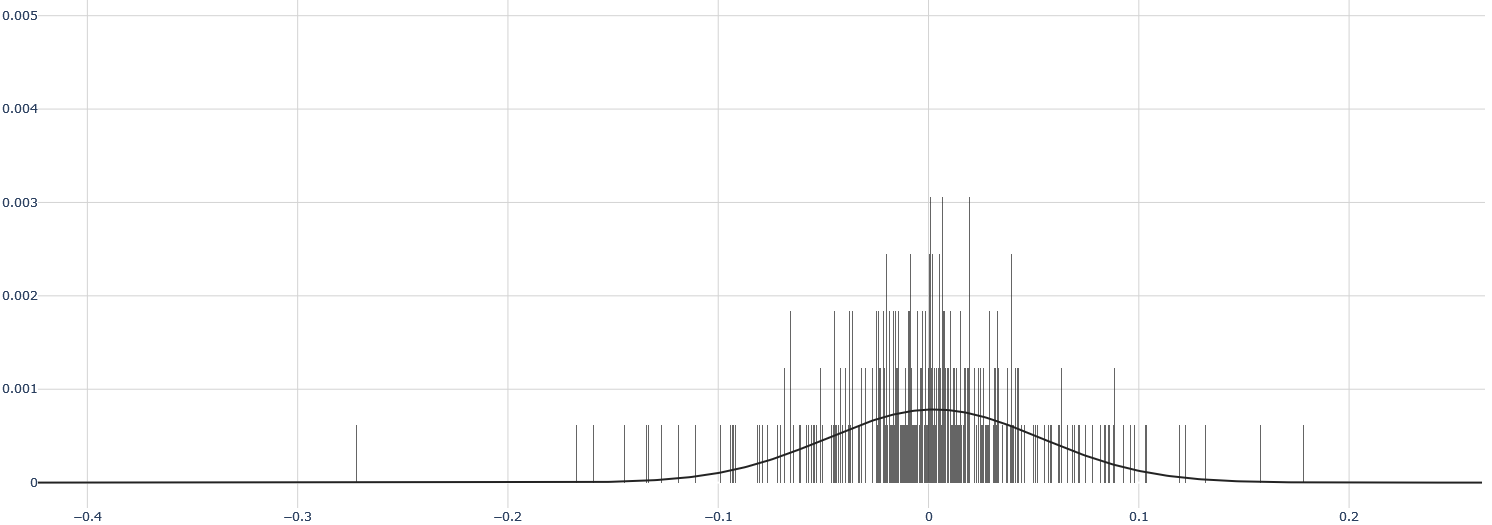

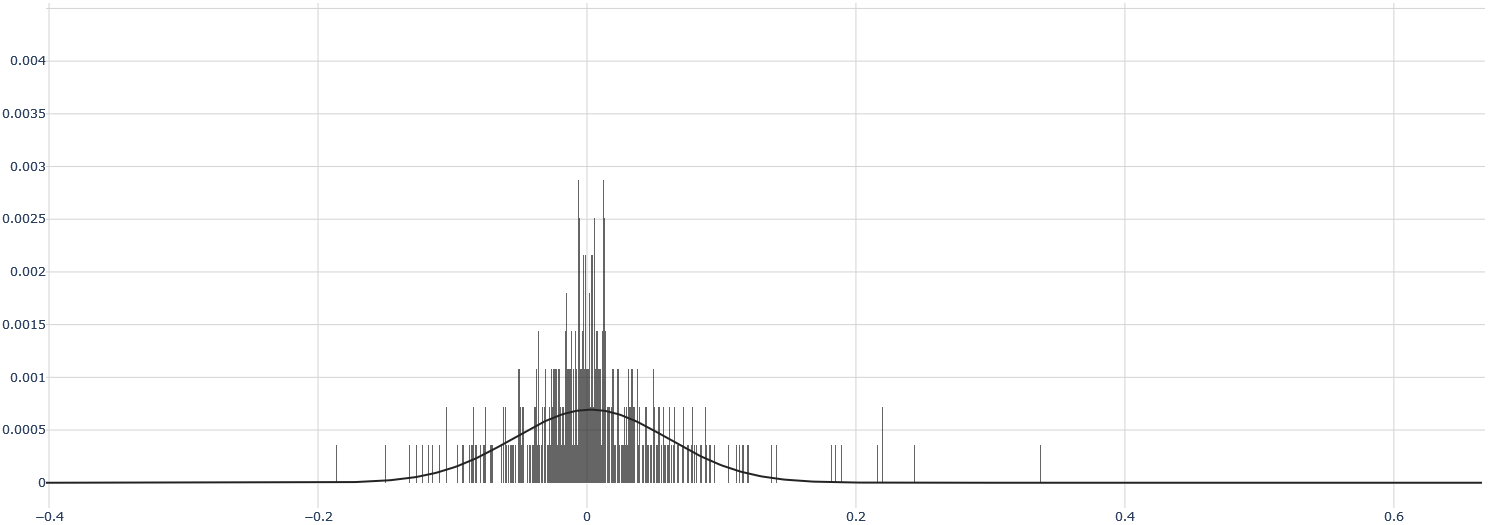

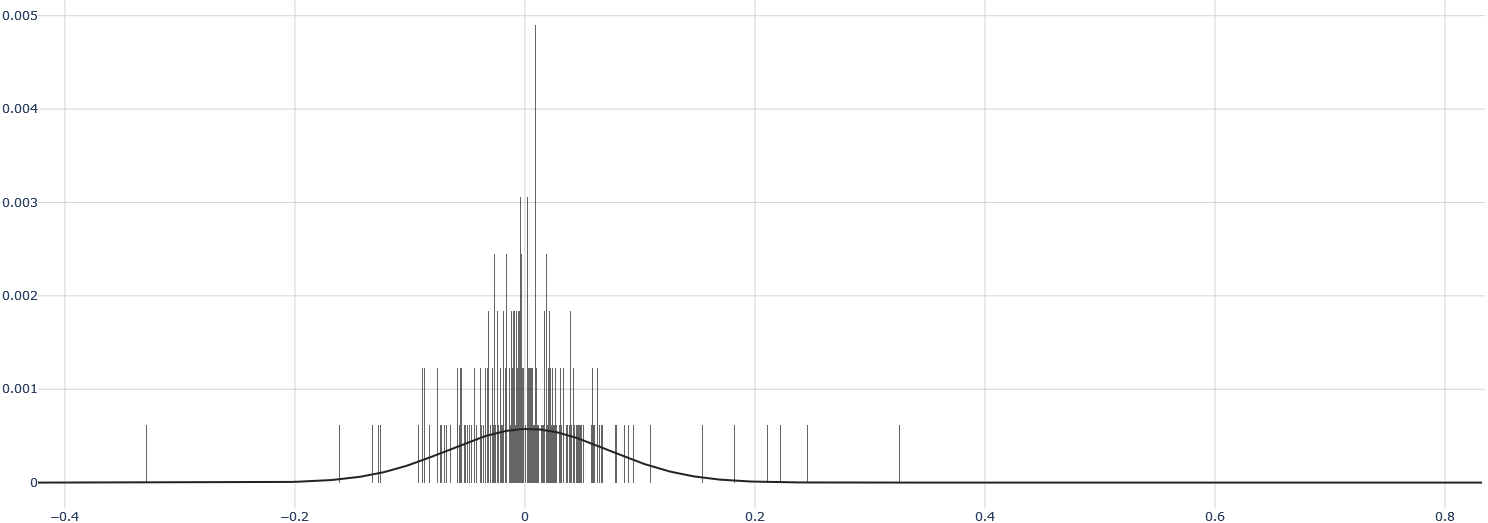

- The Louis Bachelier Model Bachelier is a pioneer of modern finance in the sense that he was the first to use Brownian motion in modeling stock prices, five years before [Einstein, 1956]. From his model, the Wiener process [Wiener, 1976] would later be formalized. The model simply explains that the stock market follows a Gaussian distribution. Of course, such a model today would not be considered rigorous, but for its time, it was already remarkably close to a correct model. Indeed, Brownian motion applied to stock price fluctuations is based on questionable assumptions: Markov chain (memoryless process), stationarity (constant mean and standard deviation), and normal distribution. We can clearly see, for example, for the four largest cryptocurrencies, that the distribution of daily returns is not really Gaussian:

<details>

<summary>extracted/6391907/images/dist-btc.png Details</summary>

### Visual Description

## Histogram: Distribution Plot

### Overview

The image is a histogram overlaid with a probability density function (PDF). The histogram consists of vertical bars representing the frequency distribution of data, while the PDF is a smooth curve that approximates the distribution. The data appears to be centered around zero.

### Components/Axes

* **X-axis:** Ranges from approximately -0.3 to 0.25, with tick marks at -0.3, -0.2, -0.1, 0, 0.1, and 0.2.

* **Y-axis:** Ranges from 0 to 0.004, with tick marks at 0, 0.0005, 0.001, 0.0015, 0.002, 0.0025, 0.003, 0.0035, and 0.004.

* **Histogram:** The histogram is represented by gray vertical bars. The height of each bar indicates the frequency of data points within that bin.

* **PDF:** A black curve is overlaid on the histogram, representing the probability density function. It approximates the shape of the histogram.

### Detailed Analysis

* **Histogram:** The histogram shows a high concentration of data points around zero. The frequency decreases as you move away from zero in either direction. The bars are densest and tallest near zero, indicating a high frequency of values close to zero.

* **PDF:** The PDF curve is centered around zero and has a bell-like shape, suggesting a normal distribution. The peak of the curve is at zero, corresponding to the highest frequency in the histogram. The curve tapers off symmetrically on both sides.

### Key Observations

* The data is heavily concentrated around zero.

* The distribution appears to be approximately normal.

* There are fewer data points in the tails of the distribution (i.e., far from zero).

### Interpretation

The histogram and PDF suggest that the data is normally distributed with a mean close to zero. The high concentration of data points around zero indicates that values close to zero are much more common than values far from zero. This type of distribution is often seen in situations where values are expected to cluster around a central value, such as measurement errors or random fluctuations around an average. The symmetry of the distribution suggests that positive and negative deviations from zero are equally likely.

</details>

Figure 17: Distribution of daily returns for BTC/USD

<details>

<summary>extracted/6391907/images/dist-eth.png Details</summary>

### Visual Description

## Histogram with Normal Distribution Overlay

### Overview

The image is a histogram overlaid with a normal distribution curve. The histogram consists of vertical lines representing the frequency of data points within specific bins. The normal distribution curve is a smooth line that approximates the distribution of the data.

### Components/Axes

* **X-axis:** Ranges from -0.4 to 0.2, with tick marks at -0.4, -0.3, -0.2, -0.1, 0, 0.1, and 0.2.

* **Y-axis:** Ranges from 0 to 0.005, with tick marks at 0, 0.001, 0.002, 0.003, 0.004, and 0.005.

* **Histogram:** Represented by vertical lines. The height of each line indicates the frequency of data points within that bin.

* **Normal Distribution Curve:** A black line that approximates the distribution of the data. It is centered around 0 and has a bell shape.

### Detailed Analysis

* **Histogram:** The vertical lines are concentrated around 0, indicating that most of the data points are clustered around this value. The frequency decreases as you move away from 0 in either direction.

* **Normal Distribution Curve:** The curve is centered around 0 and has a bell shape. It closely follows the distribution of the histogram, indicating that the data is approximately normally distributed.

* **X-Axis Values:**

* -0.4

* -0.3

* -0.2

* -0.1

* 0

* 0.1

* 0.2

* **Y-Axis Values:**

* 0

* 0.001

* 0.002

* 0.003

* 0.004

* 0.005

### Key Observations

* The data is approximately normally distributed, as indicated by the close fit between the histogram and the normal distribution curve.

* The data is centered around 0, with most of the data points clustered around this value.

* There are some outliers, as indicated by the vertical lines that are far away from 0.

### Interpretation

The histogram and normal distribution curve suggest that the data is approximately normally distributed with a mean of 0. This could represent a variety of phenomena, such as measurement errors, random fluctuations, or the distribution of a population around a central value. The outliers could represent unusual events or errors in the data. The image provides a visual representation of the distribution of the data and allows for a quick assessment of its properties.

</details>

Figure 18: Distribution of daily returns for ETH/USD

<details>

<summary>extracted/6391907/images/dist-ltc.png Details</summary>

### Visual Description

## Histogram: Distribution Plot

### Overview

The image is a histogram displaying the distribution of a dataset. The histogram consists of vertical bars representing the frequency of data points within specific ranges, overlaid with a black curve that approximates the distribution. The data appears to be centered around zero, with a concentration of values near the center and tapering off towards the extremes.

### Components/Axes

* **X-axis:** Ranges from -0.4 to 0.6, with tick marks at -0.4, -0.2, 0, 0.2, 0.4, and 0.6. The x-axis represents the values of the data being distributed.

* **Y-axis:** Ranges from 0 to 0.004, with tick marks at 0, 0.0005, 0.001, 0.0015, 0.002, 0.0025, 0.003, 0.0035, and 0.004. The y-axis represents the frequency or density of the data.

* **Bars:** Gray vertical bars represent the frequency of data points within specific ranges along the x-axis. The height of each bar corresponds to the frequency of data within that range.

* **Curve:** A black curve is overlaid on the histogram, approximating the distribution of the data. It appears to be a normal distribution curve, centered around zero.

### Detailed Analysis

* The highest frequency of data points occurs around x = 0. The bars are densest and tallest in this region.

* The frequency of data points decreases as you move away from x = 0 in either direction. The bars become shorter and sparser.

* The black curve closely follows the shape of the histogram, indicating a good fit for the distribution.

* The distribution appears to be roughly symmetrical around x = 0.

* The maximum value of the distribution is approximately 0.003.

### Key Observations

* The data is heavily concentrated around zero.

* The distribution is approximately normal.

* There are few data points beyond x = -0.2 and x = 0.2.

### Interpretation

The histogram suggests that the underlying data is centered around zero and follows a roughly normal distribution. This could represent a variety of phenomena, such as measurement errors, random fluctuations, or the distribution of a variable around its mean. The concentration of data around zero indicates that values close to zero are more common than values further away. The shape of the distribution can provide insights into the nature of the data and the processes that generate it.

</details>

Figure 19: Distribution of daily returns for LTC/USD

<details>

<summary>extracted/6391907/images/dist-xrp.png Details</summary>

### Visual Description

## Histogram: Distribution Plot

### Overview

The image is a histogram overlaid with a probability density function (PDF). The histogram consists of vertical bars representing the frequency distribution of data, while the PDF is a smooth curve that approximates the distribution. The data appears to be centered around zero.

### Components/Axes

* **X-axis:** Ranges from -0.4 to 0.8, with tick marks at -0.4, -0.2, 0, 0.2, 0.4, 0.6, and 0.8. The x-axis likely represents the values of the variable being measured.

* **Y-axis:** Ranges from 0 to 0.005, with tick marks at 0, 0.001, 0.002, 0.003, 0.004, and 0.005. The y-axis represents the frequency or density of the data.

* **Histogram:** A series of vertical bars, with the highest concentration of bars around 0.

* **PDF Curve:** A smooth, bell-shaped curve overlaid on the histogram, centered around 0.

### Detailed Analysis