# The Causal Round Trip: Generating Authentic Counterfactuals by Eliminating Information Loss

**Authors**:

- \nameRui Wu \emailwurui22@mail.ustc.edu.cn (\addrSchool of Management, University of Science and Technology of China)

- \nameLizheng Wang \emaillzwang@ustc.edu.cn (\addrSchool of Management, University of Science and Technology of China)

- \nameYongjun Li \emaillionli@ustc.edu.cn (\addrSchool of Management, University of Science and Technology of China)

> Corresponding author.

Abstract

Judea Pearl’s vision of Structural Causal Models (SCMs) as engines for counterfactual reasoning hinges on faithful abduction: the precise inference of latent exogenous noise. For decades, operationalizing this step for complex, non-linear mechanisms has remained a significant computational challenge. The advent of diffusion models, powerful universal function approximators, offers a promising solution. However, we argue that their standard design, optimized for perceptual generation over logical inference, introduces a fundamental flaw for this classical problem: an inherent information loss we term the Structural Reconstruction Error (SRE). To address this challenge, we formalize the principle of Causal Information Conservation (CIC) as the necessary condition for faithful abduction. We then introduce BELM-MDCM, the first diffusion-based framework engineered to be causally sound by eliminating SRE by construction through an analytically invertible mechanism. To operationalize this framework, a Targeted Modeling strategy provides structural regularization, while a Hybrid Training Objective instills a strong causal inductive bias. Rigorous experiments demonstrate that our Zero-SRE framework not only achieves state-of-the-art accuracy but, more importantly, enables the high-fidelity, individual-level counterfactuals required for deep causal inquiries. Our work provides a foundational blueprint that reconciles the power of modern generative models with the rigor of classical causal theory, establishing a new and more rigorous standard for this emerging field.

Keywords: Causal Inference, Diffusion Models, Causal Information Conservation, Structural Causal Models, Counterfactual Generation, BELM, Structural Reconstruction Error

1 Introduction

The fundamental challenge of causal inference, as articulated by rubin1974estimating, is our inability to simultaneously observe an individual’s potential outcomes. Generating authentic counterfactuals is thus the field’s grand challenge. Structural Causal Models (SCMs), introduced by pearl2009causality, provide the formal language for this pursuit. An SCM posits that an outcome $V_{i}$ is generated by a function of its parents $\mathbf{Pa}_{i}$ and a unique exogenous noise variable $U_{i}$ . This noise, $U_{i}$ , represents the primordial causal information —the collection of unobserved factors unique to an individual. This concept aligns directly with the long-standing focus in econometrics on unobserved individual heterogeneity, a central challenge in structural modeling for decades (heckman2001micro). Pearl’s framework for causal reasoning, the Abduction-Action-Prediction cycle, hinges on the fidelity of the first step: abduction. To answer any ”what if” question, one must first perfectly infer this primordial information $U_{i}$ from an observed outcome $v_{i}$ . For decades, while this theoretical blueprint was clear, its practical realization for complex, non-linear mechanisms remained a major computational hurdle, often addressed in econometrics through strong parametric assumptions or linear approximations (angrist2008mostly).

The advent of deep generative models, particularly diffusion models (ho2020denoising), offers a powerful new hope for bridging this gap. As near-universal function approximators, they possess the expressive power to learn the complex, non-linear functions that have long challenged classical methods (chao2023interventional; sanchez2022dcms). However, this promise is shadowed by a critical, yet overlooked, ”impedance mismatch.” These models were engineered for perceptual tasks like image synthesis, where visual plausibility is paramount, not for the logical rigor demanded by causal abduction. We argue that their standard design, which relies on approximate inversion schemes like DDIM (song2021denoising), is fundamentally at odds with the strict requirements of this classical causal problem.

In this work, we diagnose and resolve this conflict. We begin by giving the classic requirement for faithful abduction a modern name: Causal Information Conservation (CIC) In this work, ’Causal Information Conservation’ is defined operationally as the lossless, deterministic recovery of the exogenous noise variable $U$ . Its novelty lies in its application as a design principle and diagnostic tool for the diffusion model paradigm in causality, rather than as a formal information-theoretic quantity. Connecting this operational principle to formal measures, such as mutual information, is a compelling avenue for future research.. Our core contribution is the identification that standard diffusion models systematically violate this principle due to an inherent algorithmic flaw. We formalize this flaw as the Structural Reconstruction Error (SRE) —a quantifiable information loss that imposes a hard theoretical ceiling on the fidelity of any counterfactual generated by such methods. The SRE is not an estimation error to be solved with more data, but a structural defect in the tool itself.

To solve the long-standing challenge of operationalizing faithful abduction, we introduce BELM-MDCM. It is not merely a new model, but the first diffusion-based framework re-engineered from first principles to be causally sound. Architected around an analytically invertible sampler (liu2024belm), it is the first Zero-SRE causal framework by construction. This design choice reconciles the expressive power of modern diffusion models with the logical rigor of Pearl’s causal theory, ensuring the abduction step is lossless. Our primary contributions are therefore:

1. Diagnosing a Fundamental Barrier in a Classic Problem. We are the first to identify that standard diffusion models, when applied to the classic problem of SCM abduction, suffer from a structural flaw we term the Structural Reconstruction Error (SRE), which violates the foundational principle of Causal Information Conservation.

1. Proposing the First Causally-Sound Diffusion Framework. We introduce BELM-MDCM, the first framework to eliminate SRE by design. By leveraging an analytically invertible mechanism, it ensures that the power of diffusion models can be applied to causality without compromising the integrity of the abduction process.

1. Developing a Principled Methodology to Operationalize the Framework. To make our Zero-SRE framework practical and robust, we introduce two synergistic innovations: a Targeted Modeling strategy to manage complexity and a Hybrid Training Objective to provide a strong causal inductive bias, both supported by our theoretical analysis.

Through a comprehensive experimental evaluation, we demonstrate that BELM-MDCM not only sets a new state-of-the-art in estimation accuracy but, more critically, unlocks the generation of authentic individual-level counterfactuals for deep causal inquiries. By providing a foundational blueprint that resolves a core tension between modern machine learning and classical causal theory, our work establishes a new, more rigorous standard for this research direction.

1.1 The Inversion Challenge in Diffusion-Based Causality

Diffusion models (ho2020denoising) are powerful generative models that learn to reverse a fixed, gradual noising process. They train a neural network, $\epsilon_{\theta}(\mathbf{x}_{t},t)$ , to predict the noise component of a corrupted sample $\mathbf{x}_{t}$ by optimizing a simple mean-squared error objective:

$$

\begin{split}L_{\text{simple}}(\theta)=\mathbb{E}_{t,\mathbf{x}_{0},\boldsymbol{\epsilon}}\bigg[\Big\|\boldsymbol{\epsilon}-\epsilon_{\theta}\big(\sqrt{\bar{\alpha}_{t}}\mathbf{x}_{0}+\sqrt{1-\bar{\alpha}_{t}}\boldsymbol{\epsilon},t\big)\Big\|^{2}\bigg]\end{split} \tag{1}

$$

where $\bar{\alpha}_{t}$ defines the noise schedule and $\boldsymbol{\epsilon}\sim\mathcal{N}(\mathbf{0},\mathbf{I})$ . This trained network is then used to iteratively denoise a variable from pure noise back to a clean sample. A standard deterministic method for this generative process is the Denoising Diffusion Implicit Model (DDIM) (song2021denoising):

$$

\begin{split}\mathbf{x}_{t-1}=\sqrt{\bar{\alpha}_{t-1}}\left(\frac{\mathbf{x}_{t}-\sqrt{1-\bar{\alpha}_{t}}\epsilon_{\theta}(\mathbf{x}_{t},t)}{\sqrt{\bar{\alpha}_{t}}}\right)+\sqrt{1-\bar{\alpha}_{t-1}}\cdot\epsilon_{\theta}(\mathbf{x}_{t},t)\end{split} \tag{2}

$$

However, causal abduction requires the inverse operation: encoding an observed data point $\mathbf{x}_{0}$ into its latent noise code $\mathbf{x}_{T}$ . Standard frameworks (chao2023interventional) use the DDIM inversion, which only approximates this path:

$$

\begin{split}\mathbf{x}_{t+1}=\sqrt{\bar{\alpha}_{t+1}}\left(\frac{\mathbf{x}_{t}-\sqrt{1-\bar{\alpha}_{t}}\epsilon_{\theta}(\mathbf{x}_{t},t)}{\sqrt{\bar{\alpha}_{t}}}\right)+\sqrt{1-\bar{\alpha}_{t+1}}\cdot\epsilon_{\theta}(\mathbf{x}_{t},t)\end{split} \tag{3}

$$

This inversion is approximate because it relies on the noise prediction $\epsilon_{\theta}(\mathbf{x}_{t},t)$ remaining constant across the step, which introduces discretization errors that accumulate (liu2022pseudo). This structural flaw, which we term the Structural Reconstruction Error (SRE), systematically corrupts the inferred exogenous noise $U_{i}$ . The initial error in the abduction step then propagates through the entire Abduction-Action-Prediction cycle, compromising the fidelity of the final counterfactual.

1.2 Our Solution: A Zero-SRE Causal Framework

To eliminate SRE by construction, we build our framework upon an analytically invertible sampler: the B idirectional E xplicit L inear M ulti-step (BELM) sampler (liu2024belm). BELM overcomes the ”memoryless” limitation of single-step samplers like DDIM by using a history of noise predictions, a principle grounded in classical theory for solving ODEs (hairer2006solving).

Specifically, we employ a second-order BELM. During decoding, it computes a more stable effective noise, $\boldsymbol{\epsilon}_{\text{eff}}$ , using predictions from the current and previous timesteps:

$$

\boldsymbol{\epsilon}_{\text{eff}}=\frac{3}{2}\epsilon_{\theta}(\mathbf{x}_{t},t)-\frac{1}{2}\epsilon_{\theta}(\mathbf{x}_{t+1},t+1) \tag{4}

$$

This improved estimate is then used in a DDIM-like update. The key innovation is that the corresponding encoding process is constructed to be the exact algebraic inverse of this decoding process, guaranteeing that the round-trip is lossless, i.e., $\mathbf{H}(\mathbf{T}(\mathbf{x}_{0}))=\mathbf{x}_{0}$ . While the original work on BELM focused on general generative tasks, we are the first to identify, leverage, and theoretically justify its analytical invertibility as the key to satisfying the principle of Causal Information Conservation for rigorous counterfactual generation. Our choice of a second-order BELM represents a deliberate trade-off, providing substantial accuracy gains over single-step methods while maintaining practical efficiency (liu2024belm), making it ideal for our causal framework.

1.3 Methodological Gaps in Applying Invertible SCMs

However, achieving high-fidelity causal inference requires more than a simple substitution of one sampler for another. The principle of analytical invertibility, while theoretically sound, exposes new challenges in practical SCM implementation that our framework is designed to address.

The Challenge of Model Specification: Targeted Modeling.

A key decision in SCM construction is assigning a causal mechanism to each node. Naively applying a complex, computationally expensive BELM-based diffusion model to every node in the causal graph is suboptimal. This motivates our Targeted Modeling strategy, where model complexity is treated as a resource to be allocated judiciously across the graph.

The Challenge of Downstream Tasks: Hybrid Training.

The second challenge arises from a fundamental mismatch in objectives. A diffusion model is trained on a generative objective, $L_{\text{diffusion}}(\theta)$ , while a downstream predictive task is optimized using a discriminative loss, $L_{\text{task}}(\phi)$ . These two objectives are not aligned. This ”objective mismatch” motivates our Hybrid Training strategy, which seeks to unify these two goals.

2 Theoretical Analysis: An Operator-Theoretic Framework

To formalize our thesis that Causal Information Conservation is paramount and its violation via Structural Reconstruction Error is a fundamental barrier, we develop a rigorous operator-theoretic framework. This perspective is essential for analyzing the fidelity of the causal mapping process itself, moving beyond simple prediction errors. We present the first formal analysis that decomposes the counterfactual error in diffusion-based causal models to explicitly isolate the SRE, proving how our Zero-SRE design eliminates this critical structural limitation.

Our analysis first establishes the conditions for perfect counterfactual generation (§ 2.1-§ 2.3) and proves that standard methods produce a non-zero SRE, which our sampler eliminates by construction (Proposition 5 - 6; § 2.4). The centerpiece is a novel error decomposition theorem that isolates the SRE, motivating our Zero-SRE design (§ 2.5-§ 2.7). We conclude with learnability guarantees and a discussion of implications for advanced causal tasks like transportability (§ 2.8-§ 2.10).

2.1 Problem Formulation and Causal Operators

Let $(\Omega,\mathcal{F},P)$ be a probability space. We consider endogenous variables $\mathbf{V}$ as elements of the Hilbert space of square-integrable random variables, $\mathcal{X}:=L^{2}(\Omega,\mathbb{R}^{d})$ . Unless otherwise specified, all vector norms $\|·\|$ in the subsequent analysis refer to the standard Euclidean ( $L_{2}$ ) norm.

**Definition 1 (Functional SCM Operator)**

*A Structural Causal Model is defined by a set of unknown, true functional operators $\{\mathbf{F}_{i}\}_{i=1}^{d}$ , where each $\mathbf{F}_{i}:\mathcal{X}^{\text{pa}_{i}}×\mathcal{U}_{i}→\mathcal{X}_{i}$ is a map such that $V_{i}:=\mathbf{F}_{i}(\mathbf{Pa}_{i},U_{i})$ , with $\mathbf{Pa}_{i}$ being the set of parent random variables and $U_{i}$ an exogenous noise variable. We establish the convention that the corresponding lowercase bold letter, $\mathbf{pa}_{i}$ , denotes a specific vector of observed values for these parents.*

Our goal is to learn a model parameterized by $\theta$ that approximates this SCM. Our model consists of a pair of conditional operators for each variable $V_{i}$ :

1. A decoder (generative) operator $\mathbf{H}_{\theta}:\mathcal{U}×\mathcal{X}^{p}→\mathcal{X}$ , which aims to approximate $\mathbf{F}$ .

1. An encoder (inference) operator $\mathbf{T}_{\theta}:\mathcal{X}×\mathcal{X}^{p}→\mathcal{U}$ , which aims to perform abduction by inferring the latent noise.

These operators are realized by solving the probability flow ODE (Appendix A). The decoder $\mathbf{H}_{\theta}$ solves the ODE from $t=T$ to $t=0$ , while the encoder $\mathbf{T}_{\theta}$ solves it from $t=0$ to $t=T$ . Our BELM sampler is a high-fidelity numerical solver designed such that these forward and backward operations are exact algebraic inverses.

2.2 Identifiability and Exact Counterfactual Generation

We adapt principles from identifiable generative modeling (chao2023interventional) to formalize the conditions for exact counterfactuals. This requires assuming the SCM is invertible with respect to its noise term, a condition discussed in Section 2.11.

**Theorem 2 (Identifiability via Statistical Independence)**

*Given an SCM operator $X:=\mathbf{F}(\mathbf{Pa},U)$ where $U\perp\!\!\!\perp\mathbf{Pa}$ and $\mathbf{F}$ is invertible w.r.t. $U$ . If a learned encoder $\mathbf{T}_{\theta}$ (with sufficient capacity) yields a latent representation $Z=\mathbf{T}_{\theta}(X,\mathbf{Pa})$ that is statistically independent of the parents $\mathbf{Pa}$ , then $Z$ is an isomorphic representation of the exogenous noise $U$ .*

2.3 Geometric Inductive Bias for Identifiability

The score-matching objective’s geometric inductive biases strengthen our identifiability argument. We leverage the principle of implicit regularization, where optimizers favor ”simpler” functions (hochreiter1997flat; neyshabur2018pac). We adopt the principle of simplicity bias, a cornerstone of modern deep learning theory that, while empirically supported, remains an active and not yet universally proven area of research. Our conclusions are conditioned on its validity, as discussed further in Section 2.11. This suggests the model learns the most parsimonious geometric transformation required to explain the data.

Considering the local geometry of the data density $p(\mathbf{x})$ provides powerful intuition. In a local region $\mathcal{R}$ , if the data is isotropic (spherically symmetric), the simplest score function is a radial vector field, yielding a conformal map. If the structure is simply anisotropic (e.g., ellipsoidal), the model is biased towards learning a local affine map. This refines the notion of a purely conformal bias and leads to the following proposition.

**Proposition 3 (Implicit Bias towards Simple Geometric Maps)**

*Assume (A1) the true data density $p(\mathbf{x})$ is smooth ( $C^{2}$ ) and (A2) the optimization process has a simplicity bias (e.g., favoring low-complexity solutions, see Appendix H).

1. If there exists a local region $\mathcal{R}$ where $p(\mathbf{x})$ is isotropic, the optimal learned score function is a radial vector field, and the flow map it generates is a conformal map on $\mathcal{R}$ .

1. If we relax the condition to a local region $\mathcal{R}$ where $p(\mathbf{x})$ has an ellipsoidal structure, the optimal learned score function is normal to the ellipsoidal iso-contours, and the flow map it generates is a local affine transformation on $\mathcal{R}$ .*

The formal argument is detailed in Appendix H. This proposition is significant: it suggests that the model defaults to learning the most parsimonious, well-behaved, and locally invertible map that can explain the data’s geometry. This bias is crucial for the abduction step, as it prevents the pathological distortions that would corrupt the inferred causal noise $U$ .

**Theorem 4 (Operator Isomorphism Guarantees Exact Counterfactuals)**

*Let the conditions of Theorem 2 hold. If the learned operator pair $(\mathbf{T}_{\theta},\mathbf{H}_{\theta})$ constitutes a conditional isomorphism (i.e., $\mathbf{H}_{\theta}(\mathbf{T}_{\theta}(·,\mathbf{pa}),\mathbf{pa})=\mathbf{I}$ , the identity operator), then the model’s prediction under an intervention $do(\mathbf{Pa}:=\boldsymbol{\alpha})$ is exact.*

Proof A full proof, covering cases for different dimensions of the exogenous noise variable, is provided in Appendix B.

2.4 Analysis of Inversion Fidelity

We now formally analyze the inversion error. We prove that standard approximate schemes produce a non-zero SRE (Proposition 5), whereas our chosen sampler eliminates it by construction (Proposition 6).

**Proposition 5 (Structural Error of Approximate Inversion)**

*Let $\mathbf{T}_{\text{DDIM}}$ be the operator for one step of DDIM inversion from $\mathbf{x}_{t}$ to $\mathbf{x}_{t+1}$ , and $\mathbf{H}_{\text{DDIM}}$ be the generative step operator from $\mathbf{x}_{t+1}$ to $\mathbf{x}_{t}$ . The single-step reconstruction error is non-zero and of second order in the time step $\Delta t$ :

$$

(\mathbf{H}_{\text{DDIM}}\circ\mathbf{T}_{\text{DDIM}})(\mathbf{x}_{t})-\mathbf{x}_{t}=\mathcal{O}((\Delta t)^{2})

$$

This error accumulates over the full trajectory, leading to a non-zero Structural Reconstruction Error.*

Proof See Appendix C for a rigorous proof.

**Proposition 6 (Analytical Invertibility of the Sampler)**

*Let $\mathbf{T}_{\text{BELM}}$ and $\mathbf{H}_{\text{BELM}}$ be the operators corresponding to the full-trajectory BELM sampler for inference and generation, respectively. For a fixed noise prediction network $\epsilon_{\theta}$ , the operators are exact algebraic inverses:

$$

\mathbf{H}_{\text{BELM}}\circ\mathbf{T}_{\text{BELM}}=\mathbf{I}

$$*

Proof The proof follows from the algebraic construction of the BELM update rules, as detailed in Appendix C.

2.5 Error Decomposition for Counterfactual Estimation

This brings us to our central theoretical result: an error decomposition theorem that rigorously partitions the total counterfactual error. This decomposition isolates the SRE and mathematically demonstrates why its elimination is critical.

**Definition 7 (Counterfactual Error Components)**

*We formally define the two primary sources of error in counterfactual estimation for the invertible case:

1. The Structural Reconstruction Error ( $E_{SR}$ ) measures the information loss from the model’s abduction-action cycle on a given sample $X$ :

$$

E_{SR}(X):=\|(\mathbf{H}_{\theta}\circ\mathbf{T}_{\theta}-\mathbf{I})X\|^{2}

$$

1. The Latent Space Invariance Error ( $E_{LSI}$ ) measures the failure of the learned latent space to remain invariant under interventions on parent variables:

$$

E_{LSI}:=\|\mathbf{T}_{\theta}(X,\mathbf{Pa})-\mathbf{T}_{\theta}(X_{\boldsymbol{\alpha}}^{\text{true}},\boldsymbol{\alpha})\|^{2}

$$*

**Theorem 8 (Counterfactual Error Bound)**

*Let a model be defined by $(\mathbf{T}_{\theta},\mathbf{H}_{\theta})$ and the true SCM by $\mathbf{F}$ . Assume the decoder $\mathbf{H}_{\theta}$ is $L_{\mathcal{H}}$ -Lipschitz. The expected squared error of the model’s counterfactual prediction $\hat{X}_{\boldsymbol{\alpha}}$ is bounded by the expectation of the two error components:

$$

\mathbb{E}\left[\|\hat{X}_{\boldsymbol{\alpha}}-X_{\boldsymbol{\alpha}}^{\text{true}}\|^{2}\right]\leq 2\mathbb{E}\left[E_{SR}(X_{\boldsymbol{\alpha}}^{\text{true}})\right]+2L_{\mathcal{H}}^{2}\mathbb{E}\left[E_{LSI}\right]

$$*

Proof The proof is in Appendix D.

**Remark 9 (Elimination of Structural Error)**

*By Proposition 6, the Structural Reconstruction Error for BELM-MDCM is identically zero. This is the central theoretical advantage of our framework. It disentangles the error sources, allowing us to isolate the entire modeling challenge to learning a high-quality score function ( $\epsilon_{\theta}$ ) without the confounding factor of an imperfect inversion algorithm. Any remaining error is now purely a function of statistical estimation, not a structural bias of the model itself.*

**Proposition 10 (Bound on Latent Space Invariance Error)**

*We assume the learned score network, $\boldsymbol{\epsilon}_{\theta}$ , is Lipschitz continuous, ensuring the existence and uniqueness of the probability flow ODE solution via the Picard-Lindelöf theorem. Under standard integrability conditions (Fubini’s theorem), the Latent Space Invariance Error is bounded by the expected score-matching loss:

$$

\mathbb{E}\left[E_{LSI}\right]\leq C^{\prime}\cdot\mathbb{E}\left[\|\boldsymbol{\epsilon}_{\theta}-\boldsymbol{\epsilon}^{*}\|^{2}\right]

$$

for some constant $C^{\prime}$ , where $\boldsymbol{\epsilon}^{*}$ is the true score function.*

Proof The proof is in Appendix D. This proposition formally establishes that by eliminating structural error, the causal fidelity of BELM-MDCM is directly and provably controlled by its ability to accurately learn the data’s score function.

2.6 Decomposing Error: A Motivation for Empirical Validation

The error decomposition in Theorem 8 provides a clear strategy for empirical validation by isolating two distinct error sources: the Structural Reconstruction Error ( $E_{SR}$ ) and the Latent Space Invariance Error. While developing a single score combining these is future work, these components directly motivate our empirical investigations. Our ablation study (Section 5.4.2) is designed to measure the impact of a non-zero $E_{SR}$ , while our stress-test (Section 5.4.1) probes robustness when latent space invariance is challenged by a non-invertible SCM.

2.7 Theoretical Roles of Targeted Modeling and Hybrid Training

With algorithmic error eliminated by our Zero-SRE design, the challenge becomes minimizing the modeling error ( $E_{LSI}$ ). Our two methodological innovations, Targeted Modeling and Hybrid Training, are principled strategies for this purpose.

Targeted Modeling as Formal Complexity Control.

Our Targeted Modeling strategy acts as a form of structural regularization. The finite sample bound in Theorem 15 is governed by the Rademacher complexity $\mathfrak{R}_{n}(\mathcal{F}_{\Theta})$ of the entire SCM’s hypothesis space. By assigning low-complexity models to a subset of nodes, we directly constrain the overall complexity.

**Remark 11 (Effect on Generalization Bound)**

*Our Targeted Modeling strategy is formally justified as a complexity control mechanism. The Rademacher complexity of a composite SCM is bounded by the sum of the complexities of its individual mechanisms (mohri2018foundations). By strategically substituting a high-complexity diffusion model $\mathcal{F}_{\text{diff}}$ with a lower-complexity alternative $\mathcal{F}_{\text{simple}}$ for non-critical nodes, Targeted Modeling directly minimizes this upper bound. This leads to a tighter generalization bound and improves the statistical efficiency of the overall SCM.*

Hybrid Training as a Weighted Score-Matching Objective.

The Hybrid Training Objective, $L_{\text{total}}=L_{\text{diffusion}}+\lambda· L_{\text{task}}$ , imparts a crucial inductive bias for learning a causally salient score function. The task-specific loss acts as a conductor’s baton, forcing the model to prioritize learning an accurate score function in regions of the data manifold most critical to the causal question. We formalize this by proposing that the auxiliary loss implicitly implements a weighted score-matching objective.

**Proposition 12 (Hybrid Objective as a Weighted Score-Matching Regularizer)**

*The auxiliary task loss $L_{\text{task}}$ provides a lower bound for the model’s error, weighted by a function reflecting the causal salience of the data manifold. Minimizing the hybrid objective $L_{\text{total}}$ is thereby equivalent to solving a weighted score-matching problem that prioritizes accuracy in causally salient regions, leading to a smaller effective Latent Space Invariance Error. (A rigorous proof is provided in Appendix E.)*

This proposition formally grounds our hybrid training strategy, revealing that the task-specific loss intelligently forces the diffusion model to prioritize accuracy in regions of the data manifold most critical to the causal question. This reinforces the CIC principle by avoiding information loss where it matters most, effectively implementing the simplicity bias principle from Section 2.3.

We can deepen this insight by analyzing its information-theoretic implications.

**Proposition 13 (Disentanglement via Hybrid Objective)**

*Information-theoretically, the hybrid objective provides a strong inductive bias towards learning a disentangled latent representation. It encourages a ”division of labor” where the task-specific component explains variance from the parents $\mathbf{Pa}$ , while the diffusion component’s latent code $Z=\mathbf{T}_{\theta}(V,\mathbf{Pa})$ models the residual information. This implicitly pushes $Z$ towards being independent of $\mathbf{Pa}$ , a crucial step towards satisfying the identifiability conditions.*

Proof A detailed information-theoretic argument is provided in Appendix E.

2.8 BELM-MDCM as a Unifying Framework

The principle of Causal Information Conservation also unifies our framework with classical models. Simpler models like Additive Noise Models (ANMs) can be seen as special cases where this principle is met trivially, positioning our work as a generalization of established causal principles. For instance, in a classic ANM (hoyer2009nonlinear), $V_{i}=f_{i}(\mathbf{Pa}_{i})+U_{i}$ , the noise is recovered by a direct, lossless inversion: $U_{i}=V_{i}-f_{i}(\mathbf{Pa}_{i})$ . Our framework generalizes this principle to arbitrarily complex, non-additive mechanisms, offering a flexible, non-parametric extension to classical structural equation models (wooldridge2010econometric). The importance of noise distributions, particularly non-Gaussianity, for identifiability in linear models is also a well-established principle (shimizu2006linear).

2.9 Learnability and Statistical Guarantees

We now provide finite-sample learnability guarantees for our SCM framework.

**Proposition 14 (Asymptotic Consistency)**

*Under standard regularity conditions, as the number of data samples $n→∞$ and model capacity $N→∞$ , the learned operators $(\hat{\mathbf{T}}_{n},\hat{\mathbf{H}}_{n})$ are consistent estimators of the ideal operators $(\mathbf{T}^{*},\mathbf{H}^{*})$ : $\hat{\mathbf{T}}_{n}\xrightarrow{p}\mathbf{T}^{*}$ and $\hat{\mathbf{H}}_{n}\xrightarrow{p}\mathbf{H}^{*}$ .*

**Theorem 15 (Finite Sample Bound for Causal Diffusion SCMs)**

*Let an SCM consist of $d$ endogenous nodes, with a causal graph having a maximum in-degree of $d_{in}^{max}$ . Assume each causal mechanism is implemented by a score network $\epsilon_{\theta}$ that is an $L$ -layer MLP with ReLU activations, and the spectral norm of each weight matrix is bounded by $B$ . Let the input space be appropriately normalized. Let the loss function be bounded by $M$ . Then, for the parameters $\hat{\theta}_{n}$ learned from $n$ samples, the excess risk is bounded with probability at least $1-\delta$ :

$$

R(\hat{\theta}_{n})-R(\theta^{*})\leq C\cdot\frac{d\cdot L\cdot B^{L}\cdot\sqrt{d_{in}^{max}+d_{embed}+1}}{\sqrt{n}}+M\sqrt{\frac{\log(1/\delta)}{2n}}

$$

where $C$ is a constant independent of the network architecture and sample size, and $d_{embed}$ is the dimension of the time embedding.*

Proof The proof, which combines the sub-additivity of Rademacher complexity over the SCM with standard bounds for deep neural networks (bartlett2017spectrally; neyshabur2018pac), is detailed in Appendix G.

**Remark 16 (Interpretation of the Bound)**

*This refined bound quantitatively links the generalization error to:

1. Causal Complexity ( $d·\sqrt{d_{in}^{max}}$ ): The error scales with the number of causal mechanisms ( $d$ ) and the graph’s complexity ( $d_{in}^{max}$ ), formalizing the intuition that more complex causal systems are harder to learn.

1. Network Complexity ( $L· B^{L}$ ): The error scales with the depth and spectral norm of the score networks. This provides direct theoretical grounding for our Targeted Modeling strategy, as using simpler models tightens this generalization bound.*

2.10 Implications for Causal Transportability

Causal Information Conservation also provides a foundation for transportability —applying knowledge from a source domain $\mathcal{S}$ to a target domain $\mathcal{T}$ (pearl2014transportability). Transportability requires separating invariant causal knowledge from domain-specific mechanisms. By losslessly recovering the exogenous noise $U$ (the invariant ”causal essence”), our framework achieves this separation by design; the decoders $\mathbf{H}_{\theta}$ represent the domain-specific mechanisms. This insight is formalized in the following theorem.

**Theorem 17 (Condition for Lossless Causal Transport)**

*Let a source domain $\mathcal{S}$ and a target domain $\mathcal{T}$ be described by SCMs $\mathcal{M}^{\mathcal{S}}$ and $\mathcal{M}^{\mathcal{T}}$ , respectively. Assume the following conditions hold:

1. Shared Structure: Both domains share the same causal graph $\mathcal{G}$ and the same exogenous noise distributions $\{p_{i}(U_{i})\}$ . The domains differ only in a subset of causal mechanisms $\mathcal{K}_{\text{changed}}$ .

1. Noise Independence: The exogenous noise variables $\{U_{i}\}_{i=1}^{d}$ are mutually independent.

1. Information Conservation: A model $(\mathbf{T}_{\theta},\mathbf{H}_{\theta})$ trained on data from $\mathcal{S}$ satisfies the Causal Information Conservation principle, achieving zero Structural Reconstruction Error.

Then, causal knowledge can be losslessly transported from $\mathcal{S}$ to $\mathcal{T}$ by re-learning only the operators $\{\mathbf{T}_{\theta_{k}},\mathbf{H}_{\theta_{k}}\}$ corresponding to the changed mechanisms $k∈\mathcal{K}_{\text{changed}}$ , while directly reusing all operators for invariant mechanisms.*

Proof The proof is provided in Appendix F.

2.11 Discussion of Assumptions

Our framework rests on several key assumptions, which we now critically examine.

Our geometric inductive bias argument (Proposition 3) rests on the principle of simplicity bias. While this principle is a cornerstone of modern deep learning theory with substantial empirical backing, it remains an active area of research and is not a universally proven theorem. Our conclusions are therefore conditioned on the validity of this powerful but conjectural assumption.

The cornerstone of our identifiability theory (Theorem 2) is the SCM’s invertibility with respect to its noise term $U$ . This is a strong assumption; when violated (e.g., by a many-to-one function), the abduction task becomes ill-posed.

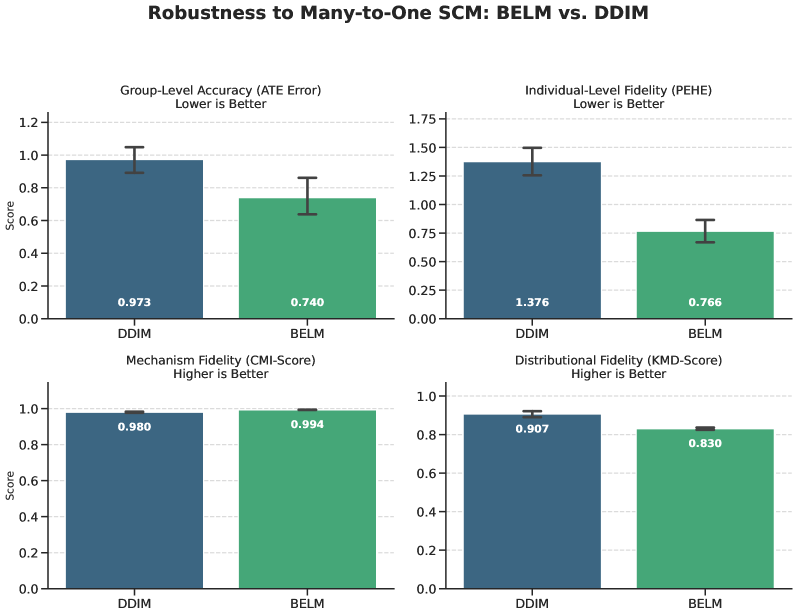

To address this foundational challenge, we provide an exhaustive theoretical treatment in Appendix C. There, we formalize the irreducible ”representational error” and derive a tighter, more general error bound (Theorem 21). More importantly, we propose a concrete mitigation strategy: a novel prior-matching regularizer (Definition 23), theoretically shown to reduce the error by encouraging the learned encoder to approximate the ideal Maximum a Posteriori (MAP) solution (Proposition 24). This highlights a primary contribution: even in the challenging non-invertible case, BELM-MDCM’s zero-SRE design eliminates the algorithmic error, thereby isolating the more fundamental representational challenge. Our stress-test in Section 5.4.1 empirically confirms this advantage, while validating our regularizer provides a clear direction for future work.

Our identifiability proof is dimension-dependent, leveraging Liouville’s theorem for $d≥ 3$ and requiring stronger assumptions like asymptotic linearity for the special case of $d=2$ . Other assumptions, such as Lipschitz continuity of the score network, are mild regularity conditions standard in deep generative model analysis and can be encouraged through architectural choices like spectral normalization.

3 Architectural Design and Training

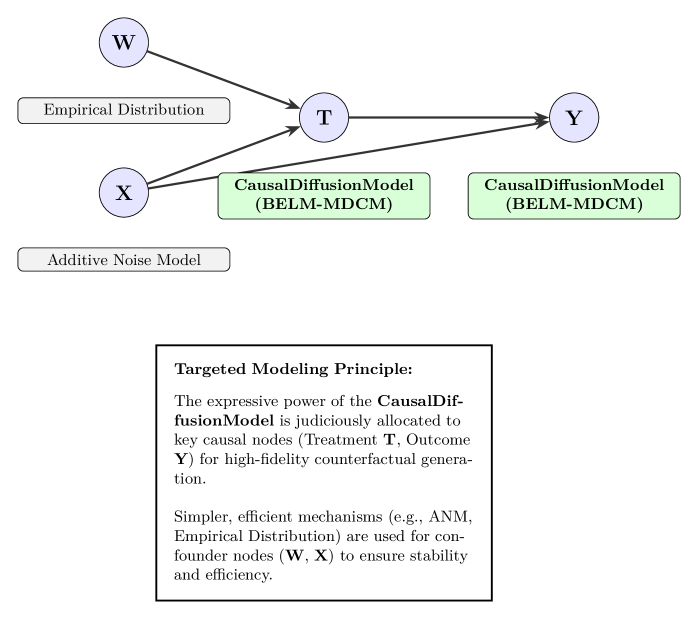

The BELM-MDCM architecture embodies our core principles through a non-monolithic, theoretically-motivated design. Its central philosophy is Targeted Modeling: judiciously allocating the expressive power of our Zero-SRE CausalDiffusionModel to nodes of causal interest (e.g., Treatment T, Outcome Y), while using simpler, efficient mechanisms for confounders, as illustrated in Figure 1. This strategy provides practical complexity control, tightening the generalization bound as established in Theorem 15.

<details>

<summary>x1.png Details</summary>

### Visual Description

## Diagram: Causal Diffusion Modeling Architecture

### Overview

The diagram illustrates a hierarchical causal modeling system with nodes representing data distributions, causal models, and noise mechanisms. Arrows indicate directional relationships and data flow between components.

### Components/Axes

- **Nodes**:

- **W**: Empirical Distribution

- **X**: Input/Founder Node

- **Y**: Outcome Node

- **T**: Treatment Node

- **Arrows**:

- **W → T**: Labeled "Empirical Distribution"

- **T → Y**: Labeled "CausalDiffusionModel (BELM-MDCM)"

- **X → T**: Labeled "CausalDiffusionModel (BELM-MDCM)"

- **X → Additive Noise Model**: Implied by connection

- **Text Box**: Contains "Targeted Modeling Principle" with explanatory text

### Detailed Analysis

1. **Empirical Distribution (W)**:

- Positioned at the top-left, feeding into Treatment (T)

- Represents observed data distribution

2. **CausalDiffusionModel (BELM-MDCM)**:

- Appears twice in the diagram:

- Between T and Y (outcome generation)

- Between X and T (treatment modeling)

- Highlighted in green boxes, emphasizing its central role

3. **Additive Noise Model**:

- Connected to X, suggesting noise injection at the input stage

4. **Targeted Modeling Principle**:

- Text box explains:

- CausalDiffusionModel's role in allocating causal nodes (T, Y)

- Use of simpler mechanisms (ANM, Empirical Distribution) for stability

- Focus on high-fidelity counterfactual generation

### Key Observations

- **Hierarchical Flow**: Data flows from empirical distribution (W) through treatment (T) to outcome (Y)

- **Dual Causal Model Usage**: BELM-MDCM operates at both treatment and outcome levels

- **Noise Injection**: Additive Noise Model modifies input (X) before processing

- **Principle Alignment**: Architecture directly implements the stated modeling philosophy

### Interpretation

This architecture demonstrates a causal inference system where:

1. Empirical data (W) is processed through a treatment model (T) using causal diffusion

2. The outcome (Y) is generated via another causal diffusion step

3. Input stability is maintained through noise modeling at the founder node (X)

4. The system prioritizes causal node allocation (T, Y) for high-fidelity generation while using simpler mechanisms for foundational stability

The diagram visually reinforces the principle that complex causal modeling (BELM-MDCM) should be reserved for key causal nodes, while simpler methods handle foundational elements. The dual use of CausalDiffusionModel suggests its versatility in different stages of the causal chain.

</details>

Figure 1: Illustration of the Targeted Modeling Principle. The expressive CausalDiffusionModel is judiciously allocated to key causal nodes (Treatment T, Outcome Y) for high-fidelity counterfactual generation. Simpler, efficient mechanisms (e.g., ANM, Empirical Distribution) are used for confounder nodes (W, X) to ensure stability and efficiency.

<details>

<summary>x2.png Details</summary>

### Visual Description

## Flowchart: Machine Learning Pipeline for Causal Identification

### Overview

The diagram illustrates a multi-stage machine learning pipeline for causal identification, structured into five phases: Pre-Processing, Embedding, Train, Post-Processing, and Results. The flow progresses left-to-right, with data transformations and model interactions depicted through interconnected blocks.

### Components/Axes

1. **Pre-Processing**

- **StandardScaler**: Standardizes numerical features (`x_num` values: 50, 257, -3.0).

- **OneHotEncoder**: Encodes categorical variables (`x_cat1`, `x_cat2`, `x_cat3` with labels: "M", "woman", and a triangle symbol).

2. **Embedding**

- **Timestep Embedding**: Processes temporal data.

- **Connection**: Combines standardized numerical (`x_num`) and encoded categorical (`x_cat`) features via a ⊕ (addition) operation.

3. **Train**

- **BELM-MDCM Module**: Trains on combined features to produce a **Noisy Target Variable**.

4. **Post-Processing**

- **Inverse Transformation**: Reverts scaled/encoded data to original space.

5. **Results**

- **Causal Identification**: Final output block.

### Detailed Analysis

- **Pre-Processing**:

- Numerical features (`x_num`) are standardized using `StandardScaler` (mean=0, std=1).

- Categorical variables (`x_cat1`, `x_cat2`, `x_cat3`) are one-hot encoded, with labels like "M" (gender), "woman" (occupation), and a triangle symbol (possibly a missing/unknown category).

- **Embedding**:

- Temporal data is embedded via `Timestep Embedding`, while numerical and categorical features are fused via element-wise addition (`x_num ⊕ x_cat`).

- **Train**:

- The **BELM-MDCM Module** (likely a hybrid model combining BERT-like language modeling with MDCM causal inference) processes the embedded data to predict a **Noisy Target Variable**.

- **Post-Processing**:

- **Inverse Transformation** undoes scaling/encoding to recover original feature scales.

- **Results**:

- **Causal Identification** block outputs the final causal relationships.

### Key Observations

1. **Data Flow**: Numerical and categorical features are preprocessed separately before being combined for training.

2. **Temporal Component**: The `Timestep Embedding` suggests time-series data is part of the input.

3. **Causal Focus**: The pipeline explicitly targets causal identification, implying the BELM-MDCM module is designed for counterfactual reasoning or causal effect estimation.

4. **Noisy Target**: The presence of a "Noisy Target Variable" indicates the model accounts for measurement error or confounding variables.

### Interpretation

This pipeline demonstrates a structured approach to causal inference in machine learning:

1. **Pre-Processing** ensures data quality by standardizing numerical features and encoding categorical variables.

2. **Embedding** integrates temporal dynamics, critical for time-dependent causal relationships.

3. **BELM-MDCM Module** likely combines deep learning (BELM) with causal modeling (MDCM) to handle complex interactions.

4. **Inverse Transformation** is essential for interpreting results in the original feature space, aiding causal interpretation.

5. The **Noisy Target Variable** suggests robustness to real-world data imperfections, a common challenge in causal analysis.

The diagram emphasizes a hybrid approach, merging statistical preprocessing, deep learning, and causal modeling to address complex, real-world datasets. The absence of explicit numerical results in the diagram implies this is a conceptual pipeline rather than an empirical study.

</details>

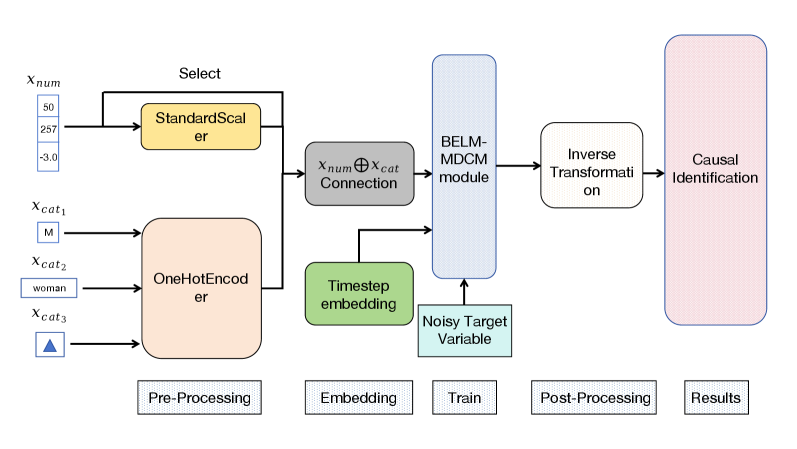

Figure 2: The detailed internal architecture of the CausalDiffusionModel. This diagram illustrates the end-to-end workflow of the causal mechanism designed for key nodes like Treatment T and Outcome Y, detailing the pre-processing, embedding, training, and post-processing stages.

The internal architecture of the CausalDiffusionModel itself, depicted in Figure 2, is engineered to learn the complex, non-linear mapping $v_{i}:=f_{i}(\mathbf{pa}_{i},u_{i})$ with high fidelity.

3.1 Mechanism for Exogenous Nodes

Exogenous nodes (without parents in the causal graph $\mathcal{G}$ ) are modeled non-parametrically via the Empirical Distribution of the observed data. This approach avoids distributional assumptions and provides a robust foundation for the Structural Causal Model (SCM).

3.2 Mechanism for Endogenous Nodes: The CausalDiffusionModel

For endogenous nodes $V_{i}$ , particularly those central to the causal query (treatment, outcome, key mediators), we employ our bespoke CausalDiffusionModel to learn the functional mapping $v_{i}:=f_{i}(\mathbf{pa}_{i},u_{i})$ .

3.2.1 Conditioning via Parent Node Transformation

The denoising process is conditioned on the parent nodes $\mathbf{pa}_{i}$ , which are transformed into a fixed-dimensional conditioning vector $\mathbf{c}∈\mathbb{R}^{d_{c}}$ . A ColumnTransformer handles heterogeneous data types: continuous parents are standardized (StandardScaler) to unify scales, while categorical parents are one-hot encoded (OneHotEncoder) to prevent artificial ordinality. The resulting vectors are concatenated into $\mathbf{c}$ , which remains constant for a given sample’s diffusion trajectory.

3.2.2 The Denoising Process

The core of the CausalDiffusionModel is a denoising network $\epsilon_{\theta}(v_{t},t,\mathbf{c})$ , implemented as a Residual MLP (he2016deep). It takes as input the noisy variable $v_{t}$ , a sinusoidal Time Embedding of timestep $t$ , and the conditioning vector $\mathbf{c}$ . Before the diffusion process, the target variable $V_{i}$ is also preprocessed (standardized for continuous values or label-encoded for categorical ones). The denoising process is driven by the BELM sampler, ensuring a mathematically exact and stable inversion path as established in Section 2.

3.2.3 Hybrid Training Objective

We introduce a Hybrid Training Objective to reconcile generative fidelity with predictive accuracy. As established in our theoretical analysis (Proposition 12), this is more than a standard multi-task learning scheme; it acts as a powerful inductive bias, creating a weighted score-matching objective that prioritizes accuracy in causally salient regions of the data manifold. The total loss is a linearly weighted combination:

$$

L_{\text{total}}=L_{\text{diffusion}}+\lambda\cdot L_{\text{task}} \tag{5}

$$

where $L_{\text{diffusion}}$ is the noise prediction error (Equation 1). The auxiliary loss $L_{\text{task}}$ is a Mean Squared Error for continuous nodes ( $L_{\text{regression}}$ ) and a Cross-Entropy loss for discrete nodes ( $L_{\text{classification}}$ ).

3.2.4 Decoding and Counterfactual Generation

For generation, the BELM sampler produces an output in the normalized space. This is then mapped back to the original data domain using the inverse transformations of the pre-fitted preprocessors (StandardScaler for continuous, LabelEncoder for categorical). For categorical outputs, the continuous value is rounded and clipped to the valid class range before the inverse mapping, ensuring that generated (counterfactual) data is interpretable and resides in the correct space.

4 New Evaluation Metrics for Generative Causal Models

The principle of Causal Information Conservation demands new evaluation dimensions that traditional metrics like ATE and PEHE cannot capture. An accurate ATE score, for instance, could arise from a model with high SRE where individual errors fortuitously cancel out at the population level. To move beyond mere outcome accuracy and directly assess a model’s adherence to our foundational principle, we propose a new, theoretically-grounded evaluation framework.

4.1 Causal Information Conservation Score (CIC-Score)

The Causal Information Conservation Score (CIC-Score) is a direct empirical diagnostic for the Structural Reconstruction Error. It quantifies a framework’s adherence to the CIC principle by disentangling algorithmic information loss (from an imperfect inversion process) from modeling error (from the statistical challenge of learning the true causal mechanism). We define the score, bounded in $[0,1]$ , using an exponential formulation:

$$

\text{CIC-Score}=\exp\left(-\left(\delta_{U}+\delta_{\text{SRE}}\right)\right)

$$

The error components are designed to isolate distinct failure modes:

- $\delta_{U}$ , the Relative Noise Recovery Error, quantifies the modeling error. It measures how well the trained network approximates the true score function, reflected in the fidelity of the recovered noise $\hat{U}$ versus the ground-truth $U_{\text{true}}$ :

$$

\delta_{U}=\frac{\mathbb{E}[\|\hat{U}_{\text{scaled}}-U_{\text{true, scaled}}\|^{2}]}{\mathbb{E}[\|U_{\text{true, scaled}}\|^{2}]}

$$

This term captures all inaccuracies from finite data and imperfect optimization.

- $\delta_{\text{SRE}}$ , the Normalized Structural Error, exclusively quantifies the algorithmic error inherent to the inversion process itself. Its definition is model-dependent to allow for fair comparisons:

- For frameworks with analytical invertibility (e.g., our BELM-MDCM, ANMs), the algorithm introduces no information loss, so we set $\delta_{\text{SRE}}\equiv 0$ by construction. Any observed reconstruction error is a symptom of modeling error, already captured by $\delta_{U}$ .

- For frameworks relying on approximate inversion (e.g., DDIM), $\delta_{\text{SRE}}$ is empirically measured to quantify this inherent algorithmic flaw:

$$

\delta_{\text{SRE}}=\frac{\mathbb{E}[\|(\mathbf{H}_{\theta}\circ\mathbf{T}_{\theta}-\mathbf{I})X\|^{2}]}{\mathbb{E}[\|X\|^{2}]}

$$

This principled decomposition allows the CIC-Score to fairly assess different frameworks by isolating structural design advantages from the universal challenge of model training.

4.2 Causal Mechanism Fidelity Score (CMF-Score)

A generative causal model’s core promise is to learn true causal mechanisms, not just outcomes. Naïve metrics like pairwise correlations fail to capture the non-linear, multi-variable, and directional nature of causality. We therefore propose the Causal Mechanism Fidelity (CMF) score, a hierarchical framework with two levels of increasing rigor.

4.2.1 Level 1 (Pragmatic): The Conditional Mutual Information Score (CMI-Score)

The Conditional Mutual Information (CMI), $I(V_{i};V_{j}|\mathbf{Pa}_{j}\setminus\{V_{i}\})$ , is a non-parametric, non-linear measure of the direct influence a parent $V_{i}$ has on its child $V_{j}$ after accounting for all other parents. The CMI-Score evaluates whether this influence is preserved. For a single mechanism $V_{j}$ , it is the average consistency across all parent-child edges:

$$

\text{CMI-Score}(V_{j})=\frac{1}{|\mathbf{Pa}_{j}|}\sum_{V_{i}\in\mathbf{Pa}_{j}}\left(1-\frac{\left|I_{\text{obs}}(V_{i};V_{j}|\cdot)-I_{\text{cf}}(V_{i};V^{\prime}_{j}|\cdot)\right|}{I_{\text{obs}}(V_{i};V_{j}|\cdot)+\epsilon}\right)

$$

where $I_{\text{obs}}$ and $I_{\text{cf}}$ are the CMI values from observational and counterfactual data, respectively. The final CMI-Score is the average over all SCM mechanisms.

4.2.2 Level 2 (Gold Standard): The Kernelized Mechanism Discrepancy (KMD) Score

To rigorously compare entire conditional distributions, we use the Maximum Mean Discrepancy (MMD) (gretton2012kernel), a kernel-based statistical test for distributional equality. The KMD-Score applies this test to the conditional distributions $p(V_{j}|\mathbf{Pa}_{j})$ that define each causal mechanism, measuring the discrepancy between the learned and observed conditionals. The final score is mapped to a similarity measure in $[0,1]$ :

$$

\text{KMD-Score}=\exp(-\gamma\cdot\mathbb{E}_{\mathbf{pa}_{j}\sim p(\mathbf{Pa}_{j})}[\text{MMD}(p(V_{j}|\mathbf{pa}_{j}),p_{\theta}(V_{j}|\mathbf{pa}_{j}))])

$$

where $\gamma$ is a scaling parameter. A score of 1 indicates that the learned conditional mechanism is statistically indistinguishable from the observed one.

Complementary and Validated Evaluation Metrics.

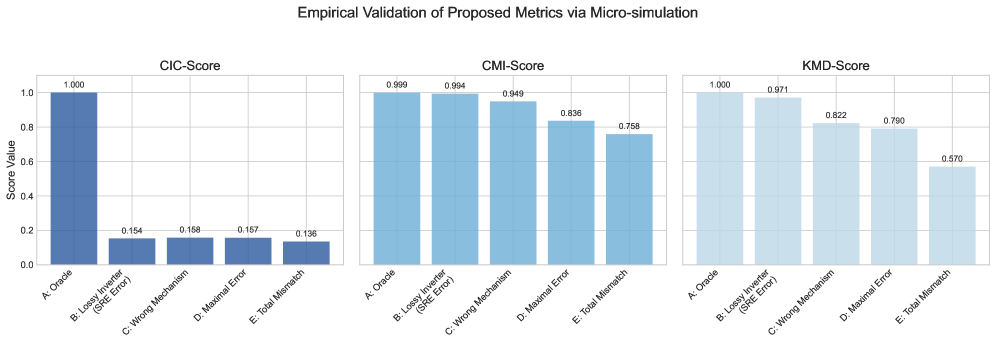

Our proposed metrics complement, rather than replace, traditional ones like ATE and PEHE. They evaluate distinct facets of performance: while ATE/PEHE measure outcome accuracy, the CMF-Score assesses mechanism fidelity. This distinction is critical, as a model can achieve a high ATE via fortuitous error cancellation despite failing to learn the true data-generating process. To ensure our metrics are practically reliable, we conducted a controlled micro-simulation study, detailed in Appendix J. The results provide strong empirical evidence for their validity and complementary roles: the CIC-Score acts as a high-sensitivity SRE detector; the CMI-Score robustly tracks the fidelity of causal associations; and the KMD-Score serves as a final arbiter of distributional similarity. This validation confirms that our evaluation framework offers a more complete, nuanced, and reliable assessment of generative causal models.

5 Experiments

Our empirical evaluation is designed as a comprehensive test of our central thesis: that eliminating SRE is a necessary condition for generating authentic counterfactuals and unlocks analytical capabilities beyond the reach of conventional methods. We structured the study as a four-act narrative to rigorously test our claims. Act I establishes our model’s state-of-the-art predictive fidelity on standard benchmarks. Act II provides a deep diagnostic analysis, using our proposed metrics as empirical evidence for the destructive effect of SRE. Act III showcases the unique capabilities unlocked by an information-conserving framework. Finally, Act IV validates the framework’s robustness through a series of stress tests and a full ablation study.

Evaluation Protocol.

For a rigorous evaluation, we employ two complementary protocols. This distinction is crucial, as it separates the assessment of our methodology’s peak performance from the diagnostic analysis of its components.

1. Ensemble Evaluation for SOTA Performance: To benchmark against state-of-the-art methods (specifically, ITE estimation in Section 5.1.3), we adopt the standard Deep Ensemble methodology. We train N=5 independent models and report the final metric (e.g., PEHE) on the ensembled prediction.

1. Individual Model Evaluation for Diagnostic Analysis: In all other experiments where the goal is a fair, apples-to-apples architectural comparison or stability assessment, we report the mean and standard deviation of metrics from individual model instances across N=5 runs. This isolates the effect of design choices from the gains of ensembling.

We estimate the Average Treatment Effect (ATE) throughout our experiments using a standard counterfactual imputation procedure, the pseudo-code for which is detailed in Algorithm 1 in Appendix K.

Baseline Estimators.

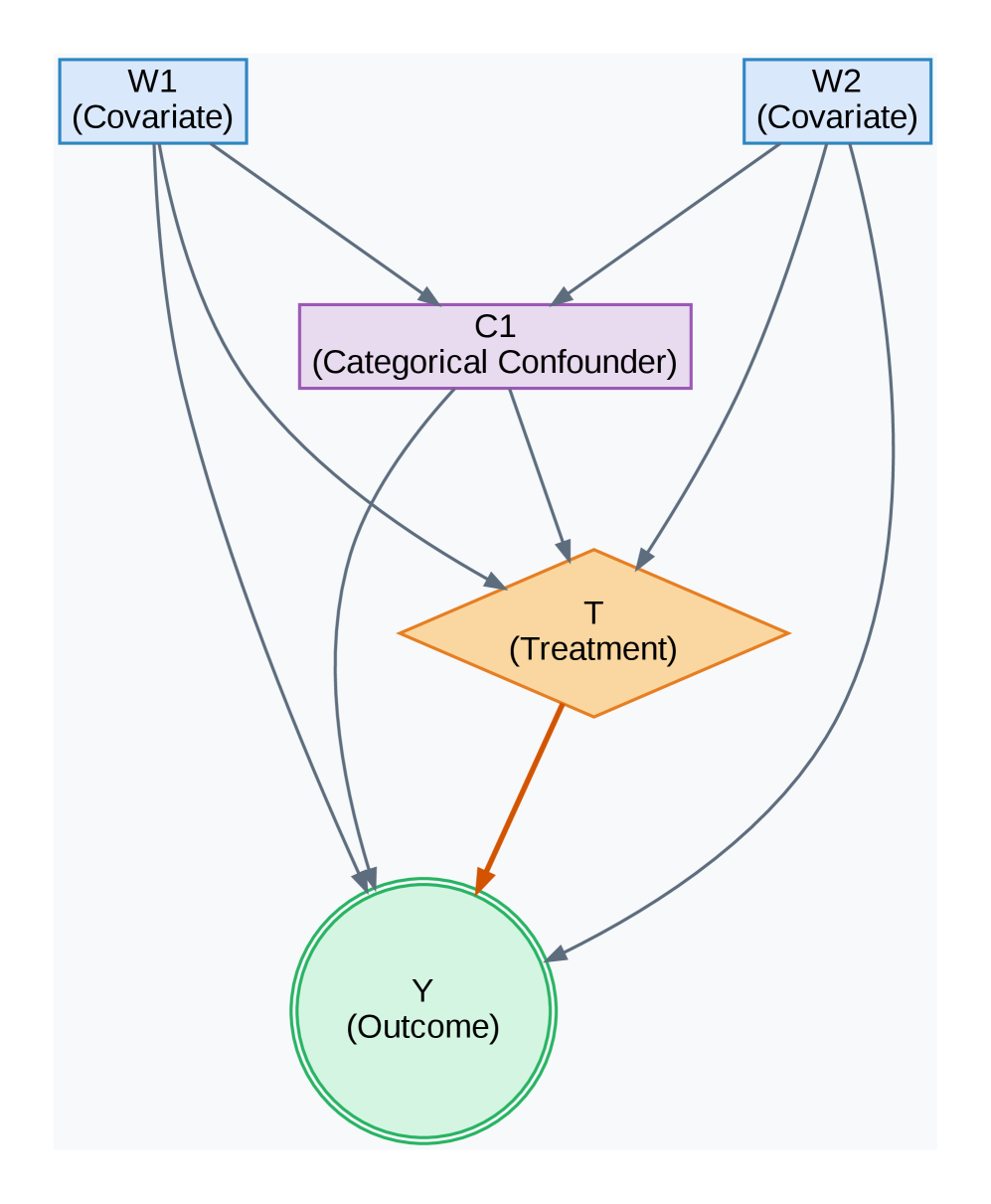

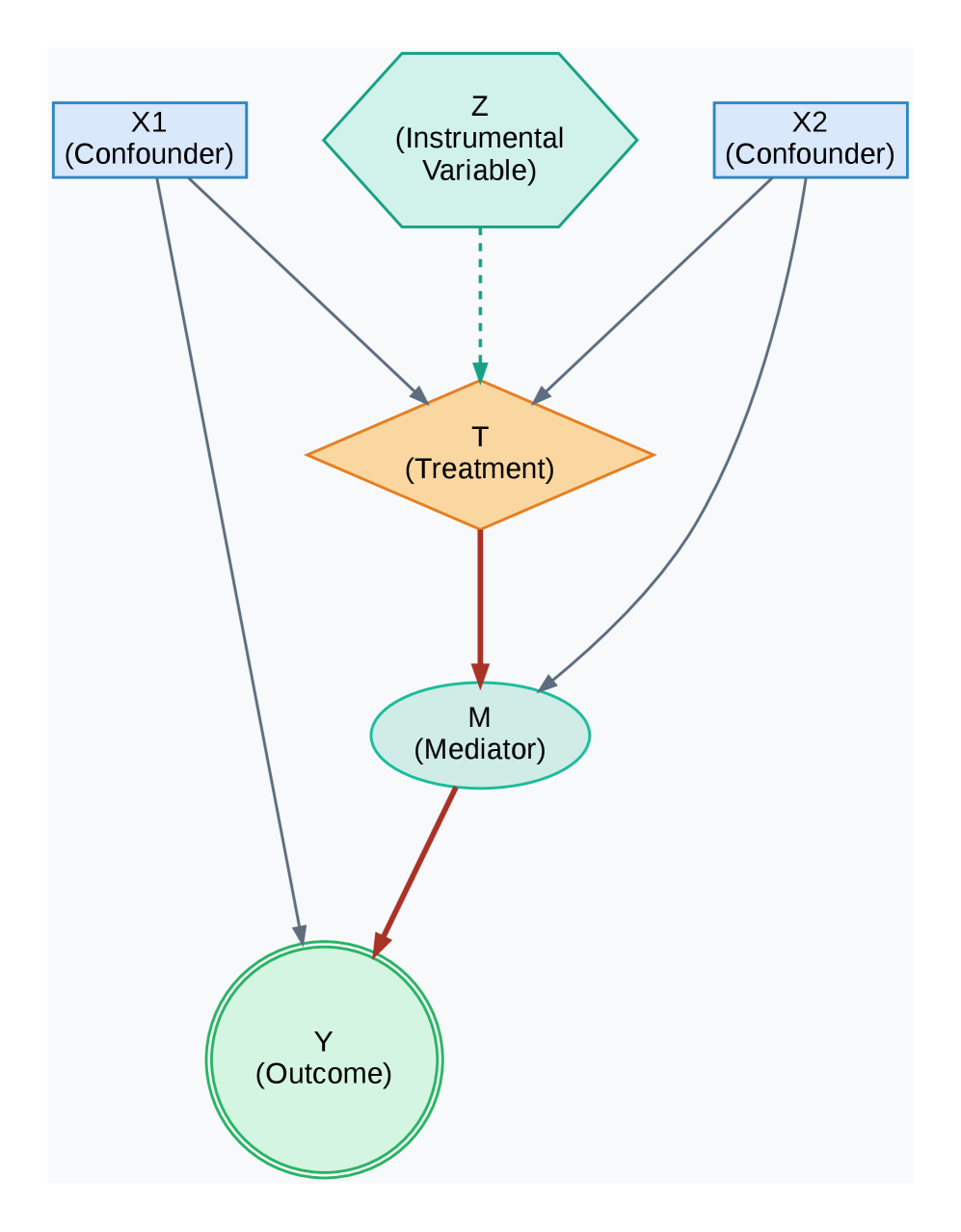

The Directed Acyclic Graphs (DAGs) for our experiments are shown in Figure 3. We benchmark BELM-MDCM against a suite of baselines from the DoWhy library (sharma2022dowhy), spanning classical statistical methods to state-of-the-art machine learning estimators to ensure a comprehensive comparison.

<details>

<summary>x3.png Details</summary>

### Visual Description

## Flowchart: Causal Relationship Diagram

### Overview

The image depicts a causal relationship diagram with five nodes connected by directional arrows. The diagram uses color-coded shapes to represent different variable types: covariates, confounders, treatments, and outcomes. Arrows indicate directional influence or dependency between components.

### Components/Axes

1. **Nodes**:

- **W1 (Covariate)**: Top-left, blue rectangle.

- **W2 (Covariate)**: Top-right, blue rectangle.

- **C1 (Categorical Confounder)**: Center, purple rectangle.

- **T (Treatment)**: Orange diamond, below C1.

- **Y (Outcome)**: Green circle, bottom-center.

2. **Arrows**:

- Gray arrows connect all nodes, indicating bidirectional or unidirectional relationships.

- Key connections:

- W1 → C1, W2 → C1 (covariates influence confounder).

- C1 → T (confounder affects treatment).

- T → Y (treatment affects outcome).

- W2 → Y (direct effect of covariate on outcome).

3. **Color Coding**:

- Blue: Covariates (W1, W2).

- Purple: Categorical confounder (C1).

- Orange: Treatment (T).

- Green: Outcome (Y).

### Detailed Analysis

- **Covariates (W1, W2)**: Positioned at the top, suggesting they are external factors influencing downstream variables.

- **Categorical Confounder (C1)**: Acts as a mediator between covariates and treatment, highlighting its role in confounding the relationship.

- **Treatment (T)**: Central node influencing the outcome, with a direct arrow from C1.

- **Outcome (Y)**: Final node with two incoming arrows (from T and W2), indicating multiple pathways to the outcome.

### Key Observations

1. **Confounder Influence**: C1 is influenced by both covariates (W1, W2) and subsequently affects the treatment (T), suggesting potential bias in causal inference if unadjusted.

2. **Direct Pathway**: W2 has a direct arrow to Y, implying a relationship independent of the confounder or treatment.

3. **Treatment-Outcome Link**: T directly impacts Y, consistent with standard causal models.

### Interpretation

This diagram illustrates a causal pathway where covariates (W1, W2) influence a categorical confounder (C1), which in turn affects treatment (T) and the outcome (Y). The direct arrow from W2 to Y suggests that W2 may have an unmediated effect on the outcome, even after accounting for C1. The structure emphasizes the importance of controlling for confounders (C1) to isolate the true effect of treatment (T) on the outcome (Y). The presence of bidirectional arrows (e.g., W2 → C1 and C1 → W2) implies potential feedback loops, though the diagram does not explicitly clarify causality directionality.

**Note**: No numerical data or trends are present; the diagram focuses on structural relationships.

</details>

(a) PSM Failure Scenario

<details>

<summary>x4.png Details</summary>

### Visual Description

## Flowchart: Causal Relationship Diagram

### Overview

The image depicts a causal relationship diagram illustrating interactions between variables in a statistical or epidemiological model. It includes confounders, an instrumental variable, treatment, mediator, and outcome, with directional arrows indicating influence.

### Components/Axes

- **Nodes**:

- **X1 (Confounder)**: Blue rectangle, positioned top-left.

- **X2 (Confounder)**: Blue rectangle, positioned top-right.

- **Z (Instrumental Variable)**: Green hexagon, centered at the top.

- **T (Treatment)**: Orange diamond, central node.

- **M (Mediator)**: Green oval, below T.

- **Y (Outcome)**: Light green circle, bottom-center.

- **Edges**:

- Solid arrows (dark gray) indicate direct causal relationships.

- Dashed arrow (light gray) from Z to T denotes indirect or instrumental influence.

- Red arrows highlight primary pathways (e.g., T → M → Y).

### Detailed Analysis

1. **Confounders (X1, X2)**:

- Both X1 and X2 directly influence T (treatment) and Y (outcome).

- No direct connection between X1 and X2.

2. **Instrumental Variable (Z)**:

- Z affects T via a dashed arrow, suggesting it modifies treatment assignment without directly impacting Y.

3. **Treatment (T)**:

- T influences M (mediator) via a solid red arrow.

- T also has a direct effect on Y (solid red arrow).

4. **Mediator (M)**:

- M is influenced by T and directly affects Y.

5. **Outcome (Y)**:

- Y receives inputs from T, M, X1, and X2.

### Key Observations

- **Confounding Bias**: X1 and X2 create bidirectional pathways to Y, indicating potential confounding effects.

- **Mediation Pathway**: T → M → Y represents a mediated effect of treatment on outcome.

- **Instrumental Variable Role**: Z’s dashed arrow to T implies it isolates exogenous variation in treatment, reducing confounding bias.

- **Direct Effects**: T and M both directly impact Y, suggesting partial mediation.

### Interpretation

This diagram models a causal pathway where confounders (X1, X2) influence both treatment (T) and outcome (Y), creating potential bias. The instrumental variable (Z) is used to address this by affecting T without directly influencing Y. The mediator (M) explains part of T’s effect on Y, while T also has a direct effect. The red arrows emphasize the primary causal chain (T → M → Y), while gray arrows show secondary relationships. This structure is typical in studies aiming to disentangle direct and indirect effects while controlling for confounding variables.

</details>

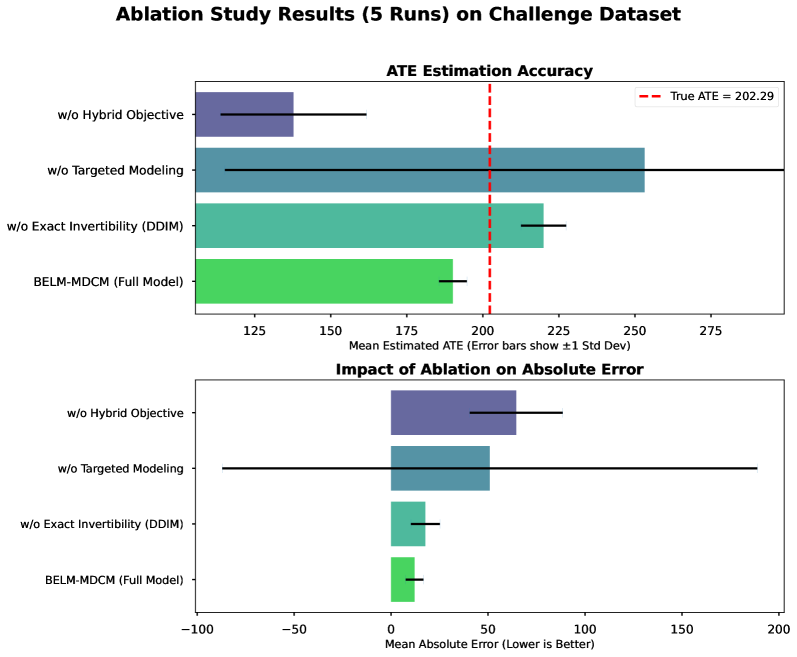

(b) Ablation Study Scenario

<details>

<summary>x5.png Details</summary>

### Visual Description

## Flowchart: Causal Relationship Diagram

### Overview

The image depicts a simplified causal flowchart illustrating relationships between confounders, treatment, and outcome variables. It uses standard flowchart notation with colored shapes and directional arrows to represent dependencies.

### Components/Axes

1. **Confounders** (Top):

- Rectangular blue box labeled "Confounders (age, educ, re74, etc.)"

- Contains variables: age, education (educ), re74 (likely a year or measurement), and unspecified additional factors

2. **Treatment** (Left):

- Orange diamond labeled "Treatment (treat)"

- Represents a decision node or intervention variable

3. **Outcome** (Bottom):

- Green circle labeled "Outcome (re78)"

- Contains the dependent variable "re78" (possibly a year or measurement)

4. **Arrows**:

- Gray arrows connect Confounders to both Treatment and Outcome

- Red arrow connects Treatment to Outcome

### Detailed Analysis

- **Confounders**: Explicitly lists age, education (abbreviated "educ"), and re74. The "etc." implies additional unlisted variables.

- **Treatment**: Positioned as a mediator between confounders and outcome.

- **Outcome**: Final node labeled "re78," suggesting a temporal or sequential relationship (e.g., re74 → re78).

- **Color Coding**:

- Blue (Confounders) → Gray arrows to Treatment/Outcome

- Orange (Treatment) → Red arrow to Outcome

- Green (Outcome)

### Key Observations

1. **Bidirectional Confounder Influence**: Confounders affect both Treatment and Outcome directly.

2. **Direct Treatment Effect**: The red arrow indicates a hypothesized causal pathway from Treatment to Outcome.

3. **Variable Naming**: Uses abbreviations (educ, re74, re78) suggesting domain-specific terminology (e.g., econometrics or social sciences).

### Interpretation

This diagram represents a **Directed Acyclic Graph (DAG)** used in causal inference analysis. It illustrates:

- **Confounder Control**: The need to account for variables like age and education that may influence both treatment assignment and outcomes.

- **Mediation Pathway**: Treatment (treat) is proposed as a direct cause of the outcome (re78), but its effect may be confounded by unmeasured variables.

- **Temporal Structure**: The use of "re74" and "re78" implies a 4-year gap, suggesting longitudinal analysis (e.g., treatment in 1974 affecting outcomes in 1978).

**Notable Design Choices**:

- Diamond shape for Treatment emphasizes its role as a decision point.

- Circular Outcome node highlights its status as the endpoint.

- Gray arrows for confounders visually subordinate them to the primary Treatment→Outcome relationship.

This structure is typical in observational studies to identify potential biases and justify adjustment methods (e.g., regression, propensity score matching).

</details>

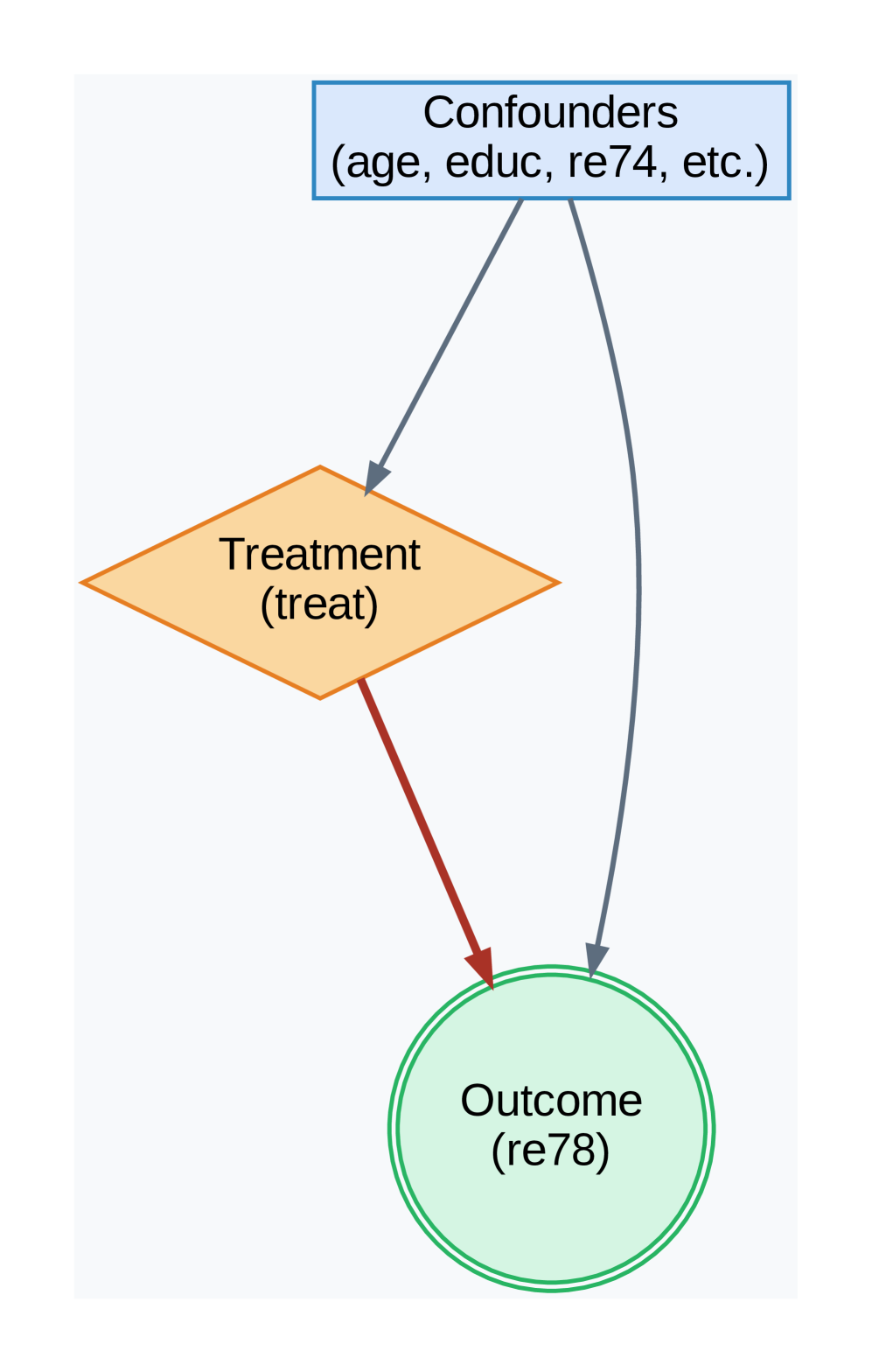

(c) Lalonde Confounding Structure

Figure 3: Directed Acyclic Graphs (DAGs) for key experiments. (a) A structure designed to challenge propensity score methods. (b) A mediation structure used for the ablation study. (c) The standard confounding structure assumed for both Lalonde-based experiments.

5.1 Act I: Establishing State-of-the-Art Predictive Fidelity

We first establish that our principled design achieves superior predictive fidelity on standard causal inference benchmarks.

5.1.1 Robustness in Non-Linear Confounding Scenarios

We tested our model in a challenging synthetic scenario (Figure 3(a)) designed with highly non-linear confounding to cause propensity-based methods to fail. Table 1 shows the results. While Causal Forest is exceptionally accurate on this specific DGP, our BELM-MDCM framework secures its position as the second most accurate method, delivering a highly stable and competitive ATE estimate. Crucially, it significantly outperforms the entire suite of propensity-based methods and powerful estimators like DML in accuracy. The high standard deviation of DML highlights its unreliability in this context, validating our model as a robust estimator where traditional approaches are compromised.

Table 1: ATE Estimation on the PSM Failure Scenario (True ATE = 5000). We report the mean ATE and standard deviation across multiple runs.

| Causal Forest | 4895.77 $±$ 69.26 | 104.23 |

| --- | --- | --- |

| Propensity Score Stratification | 5309.38 $±$ 185.36 | 309.38 |

| Linear Regression | 5348.82 $±$ 23.23 | 348.82 |

| Propensity Score Matching | 5353.93 $±$ 191.36 | 353.93 |

| Inverse Propensity Weighting | 5385.68 $±$ 52.03 | 385.68 |

| Double Machine Learning | 4285.63 $±$ 550.97 | 714.37 |

5.1.2 Accuracy and Robustness on Real-World Observational Data

We next evaluated our framework on the canonical Lalonde dataset (lalonde1986evaluating), a challenging real-world benchmark with a known RCT ground truth. Table 2 demonstrates the comprehensive superiority of our BELM-MDCM framework. It achieved a mean ATE estimate of 1567.36 $±$ 201.62, the lowest error among all methods that correctly identified the treatment effect’s positive direction. More critically, the results highlight a stark contrast in reliability. Classical methods failed entirely, while the powerful Causal Forest baseline suffered from extreme instability (Std Dev of 785.59). In contrast, BELM-MDCM exhibited remarkable robustness, with a standard deviation approximately four times lower. This outstanding performance on a canonical benchmark validates that our framework delivers accurate estimates with the consistency essential for trustworthy causal inference.

Table 2: ATE Estimation Stability on the Lalonde Dataset (RCT Benchmark ATE $≈ 1794$ ). Results for all models are reported as Mean $±$ Standard Deviation across 5 independent runs.

| Causal Forest | 1085.30 $±$ 785.59 | 708.70 |

| --- | --- | --- |

| Linear Regression | 46.33 $±$ 76.80 | 1747.67 |

| Propensity Score Matching | -3.96 $±$ 118.37 | 1797.96 |

| Propensity Score Stratification | -35.54 $±$ 81.44 | 1829.54 |

| Propensity Score Weighting | -122.55 $±$ 50.51 | 1916.55 |

| Double Machine Learning | nan $±$ nan | nan |

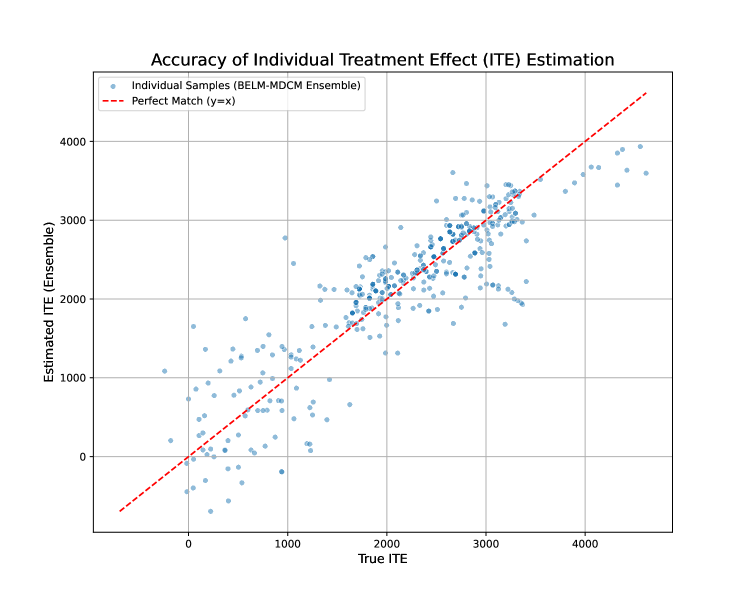

5.1.3 High-Fidelity ITE Estimation and Stability Analysis

Objective. We evaluate performance at the individual level using a semi-synthetic version of the Lalonde dataset. This experiment leverages real-world covariates and assumes the causal structure depicted in Figure 3(c). To rigorously assess both accuracy and reliability, we follow our Individual Model Evaluation protocol, reporting the mean and standard deviation of performance across 5 independent runs for each method.

Results. The PEHE results, presented in Table 3, confirm the exceptional fidelity and robustness of our framework. BELM-MDCM achieves the lowest average PEHE score of 537.84 and demonstrates remarkable stability with the lowest standard deviation of just 60.11. This performance is closely followed by Causal Forest. However, the results also highlight the instability of other meta-learners; X-Learner, in particular, exhibits extremely high variance, with a standard deviation more than three times larger than its competitors, rendering its single-run estimates unreliable. This highlights the dual advantage of our framework: superior accuracy combined with consistent, trustworthy performance. Figure 4 provides visual confirmation, showing the tight clustering of our model’s ensembled ITE estimates around the ground truth.

<details>

<summary>x6.png Details</summary>

### Visual Description

## Scatter Plot: Accuracy of Individual Treatment Effect (ITE) Estimation

### Overview

The image is a scatter plot comparing the accuracy of estimated Individual Treatment Effects (ITE) against their true values. The plot uses blue dots to represent individual samples from a BELM-MDCM ensemble and a red dashed line to indicate the "Perfect Match" (y=x), where estimated ITE equals true ITE.

### Components/Axes

- **Title**: "Accuracy of Individual Treatment Effect (ITE) Estimation" (top-center).

- **X-axis**: "True ITE" (ranging from 0 to 4000).

- **Y-axis**: "Estimated ITE (Ensemble)" (ranging from 0 to 4000).

- **Legend**:

- **Blue dots**: "Individual Samples (BELM-MDCM Ensemble)" (top-left).

- **Red dashed line**: "Perfect Match (y=x)" (top-left).

### Detailed Analysis

- **Data Points**:

- Blue dots (individual samples) are scattered across the plot, with most clustered near the red dashed line.

- Some points deviate from the line, with a few above (overestimation) and below (underestimation) the perfect match.

- The spread of points suggests variability in estimation accuracy, with no clear outliers.

- **Trends**:

- The red dashed line (y=x) acts as a reference for perfect estimation.

- The blue dots generally follow a positive linear trend, indicating that higher true ITE values correspond to higher estimated ITE values.

- The density of points increases near the line, suggesting the ensemble method performs well for mid-range ITE values.

### Key Observations

- The majority of estimated ITE values align closely with the true ITE, as seen by the concentration of blue dots near the red line.

- The spread of points indicates that while the ensemble method is generally accurate, there is some variability in estimation precision.

- No extreme outliers are visible, but the data shows a slight tendency for overestimation at higher true ITE values (points above the line).

### Interpretation

The plot demonstrates that the BELM-MDCM ensemble method provides a reliable estimation of ITE, with most individual samples closely matching the true ITE. The red dashed line (y=x) serves as a benchmark, and the proximity of blue dots to this line confirms the method's effectiveness. However, the observed spread suggests that the estimation is not perfectly consistent, potentially due to factors like sample heterogeneity or model limitations. This visualization highlights the trade-off between accuracy and variability in ITE estimation, emphasizing the need for further refinement to minimize deviations from the perfect match.

</details>

Figure 4: Accuracy of Individual Treatment Effect (ITE) Estimation on the semi-synthetic Lalonde dataset. The plot shows the ensembled estimated ITE from our model versus the true ITE. The tight clustering of our model’s estimates (blue dots) around the perfect-match line (red dash) visually demonstrates its low PEHE score.

Table 3: ITE Estimation Accuracy (PEHE) on the Semi-Synthetic Lalonde Dataset. Results are reported as Mean $±$ Standard Deviation across 5 independent runs. Lower is better.

| BELM-MDCM Causal Forest S-Learner | 537.84 $±$ 60.11 563.90 $±$ 73.66 816.26 $±$ 79.17 |

| --- | --- |

| X-Learner | 1546.38 $±$ 679.09 |

Table 4: Causal Mechanism Fidelity (CMI-Score) on the Semi-Synthetic Lalonde Dataset. Results are reported as Mean $±$ Standard Deviation across 5 runs. Higher is better.

| S-Learner BELM-MDCM Causal Forest | 0.9905 $±$ 0.0062 0.9824 $±$ 0.0092 0.9786 $±$ 0.0099 |

| --- | --- |

| X-Learner | 0.9782 $±$ 0.0145 |

| T-Learner | 0.9555 $±$ 0.0113 |

5.2 Act II: Uncovering the Accuracy-Invertibility Trade-off

We now conduct the pivotal experiment of our study: a deep diagnostic analysis using our novel CIC-Score to reveal the trade-off between predictive accuracy and mechanism invertibility. This provides the core empirical evidence for our thesis by comparing three paradigms: our BELM-MDCM (Learned Invertibility), a DDIM variant (Flawed Invertibility), and a classic RF-ANM (Assumed Invertibility).

The results in Table 5 decisively validate our framework’s principles. Our BELM-MDCM is the clear leader, achieving the lowest PEHE score (1071.95) with high stability. Critically, its CIC-Score of 0.3679 is orders of magnitude higher than the alternatives, proving its unique ability to learn an invertible mapping that conserves causal information. In stark contrast, the DDIM-MDCM model exemplifies the failure predicted by our theory: its near-zero CIC-Score confirms a near-total collapse of causal information due to SRE, leading to unreliable predictions (high PEHE and variance). The classical RF-ANM, while structurally invertible, lacks the capacity to learn the true mechanism, resulting in a zero CIC-Score and poor accuracy. This ”Golden Table” experiment underscores that both structural integrity and powerful modeling capacity are essential for high-fidelity causal inference.

Table 5: The ”Ultimate Golden Table”: A comparative analysis of model classes on predictive accuracy (PEHE) and structural integrity (CIC-Score). This table includes the NF-SCM baseline, which empirically validates the likelihood-fidelity dilemma. Results are reported as Mean $±$ Standard Deviation across 5 runs. Lower PEHE is better; higher CIC-Score is better.

| RF-ANM DDIM-MDCM NF-SCM | 1533.18 $±$ 134.24 2085.98 $±$ 788.12 442229.96 $±$ 66963.73 | 0.0000 $±$ 0.0000 0.0065 $±$ 0.0130 0.1572 $±$ 0.0232 |

| --- | --- | --- |

| BELM-MDCM | 1071.95 $±$ 152.11 | 0.3679 $±$ 0.0000 |

<details>

<summary>x7.png Details</summary>

### Visual Description

## Line Chart: Training Loss Curve

### Overview

The image depicts a line chart titled "Training Loss Curve," illustrating the progression of negative log-likelihood loss over training epochs. The chart shows a sharp initial decline in loss, followed by stabilization with minor fluctuations.

### Components/Axes

- **X-axis (Horizontal)**: Labeled "Epoch," with values ranging from 0 to 200 in increments of 25.

- **Y-axis (Vertical)**: Labeled "Negative Log-Likelihood Loss," with values ranging from -2 to 6 in increments of 2.

- **Legend**: Not visible in the image.

- **Line**: A single blue line representing the loss curve, with no markers or annotations.

### Detailed Analysis

- **Initial Phase (Epochs 0–25)**: The loss starts at approximately 6 and drops sharply to around -2 by epoch 25. This steep decline suggests rapid improvement in model performance during early training.

- **Stabilization Phase (Epochs 25–200)**: After epoch 25, the loss stabilizes near -2, with minor oscillations (approximately ±0.2). The fluctuations are consistent but do not indicate significant overfitting or underfitting.

- **Final Value**: By epoch 200, the loss remains close to -2, indicating convergence of the training process.

### Key Observations

1. **Rapid Initial Decline**: The loss decreases by ~8 units (from 6 to -2) within the first 25 epochs, highlighting the model's sensitivity to early training adjustments.

2. **Stable Convergence**: The loss plateaus near -2 after epoch 25, suggesting the model has reached a stable state with minimal further improvement.

3. **No Overfitting Signs**: The absence of a rising loss trend after stabilization implies the model generalizes well without overfitting.

### Interpretation

The chart demonstrates a typical training dynamics pattern: a steep initial drop in loss as the model learns key features, followed by stabilization as it refines its parameters. The negative log-likelihood loss approaching -2 indicates a well-trained model with low uncertainty in predictions. The lack of a legend or additional data series suggests this is a single-model evaluation. The absence of overfitting (loss does not increase post-stabilization) implies effective regularization or a well-balanced dataset. The early convergence (by epoch 25) may indicate a relatively simple problem or a highly effective learning rate schedule.

</details>

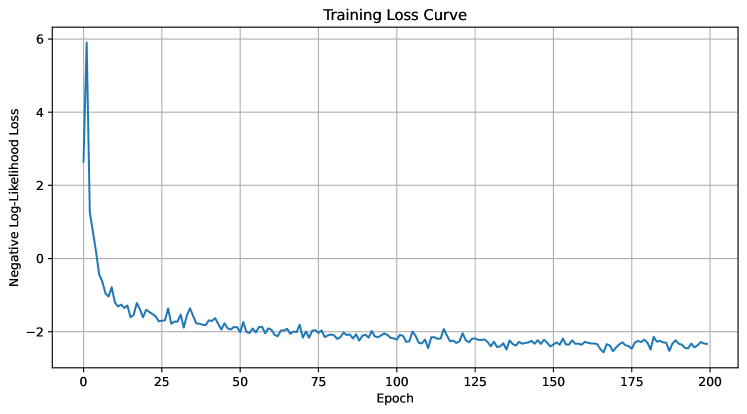

Figure 5: The training loss curve for the Conditional Normalizing Flow (NF) baseline. The smooth, stable convergence to a low negative log-likelihood value indicates a successful statistical training run. However, this did not correspond to learning the true causal mechanism, as evidenced by its extremely high PEHE score.

The Likelihood-Fidelity Dilemma: Why Natively Invertible Models Can Fail.

To rigorously test the limits of models that are natively invertible, we conducted a comprehensive stability analysis on a Conditional Normalizing Flow (NF) baseline, a model class that satisfies the Causal Information Conservation principle by construction (SRE $\equiv 0$ ). Across five independent runs with different random seeds, the NF model consistently demonstrated successful statistical learning, with its training loss stably converging to a high log-likelihood in each instance (a representative example is shown in Figure 5).

However, this statistical success was starkly contrasted by a systematic and catastrophic failure in the causal task. The model yielded an average PEHE score of 442,229.96 $±$ 66,963.73, confirming that its generated counterfactuals were fundamentally incorrect. This consistent result provides decisive evidence for a critical challenge we term the likelihood-fidelity dilemma: a model can perfectly learn to replicate a data distribution while remaining completely ignorant of the underlying causal mechanism.

The root of this dilemma is the fundamental mismatch between the optimization objective and the causal goal. The maximum likelihood objective incentivizes the NF to find any invertible mapping that transforms the data to a simple base distribution. While an infinite number of such mappings may be statistically equivalent, only one corresponds to the true, unique causal data-generating process. Without a guiding signal, the NF is mathematically predisposed to learn a causally-incorrect ”statistical shortcut.” This finding powerfully underscores the contribution of our Hybrid Training Objective. It acts as the crucial causal inductive bias that resolves this dilemma, compelling the model to learn the unique, causally salient structure and enabling valid causal inference where pure likelihood-based methods, even those with zero SRE, are destined to fail.

5.3 Act III: Unlocking Deeper Causal Inquiry with a High-Fidelity Model

An information-conserving model serves as a trustworthy ”world model” for deep causal inquiry. We showcase three applications uniquely enabled by our framework’s high-fidelity counterfactuals.

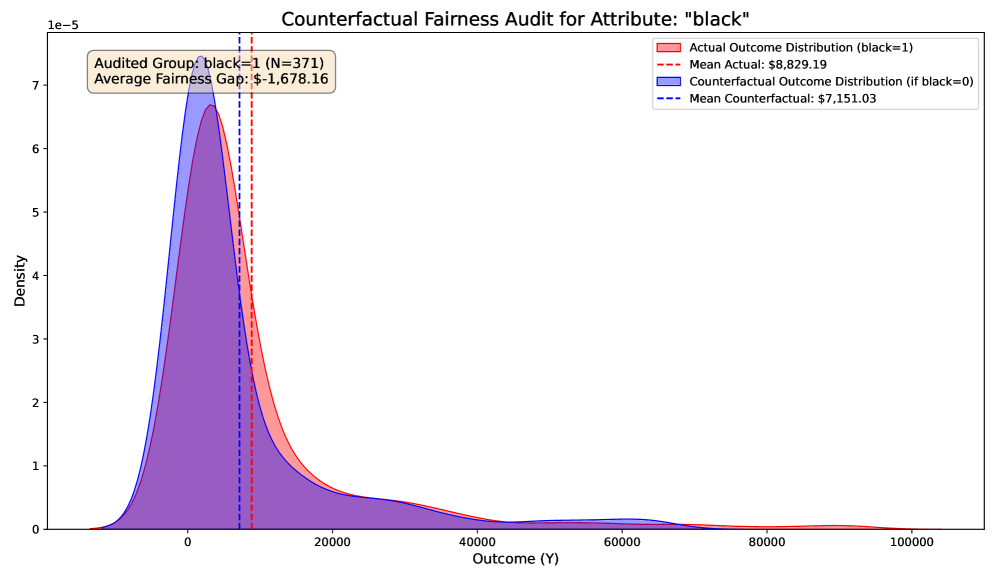

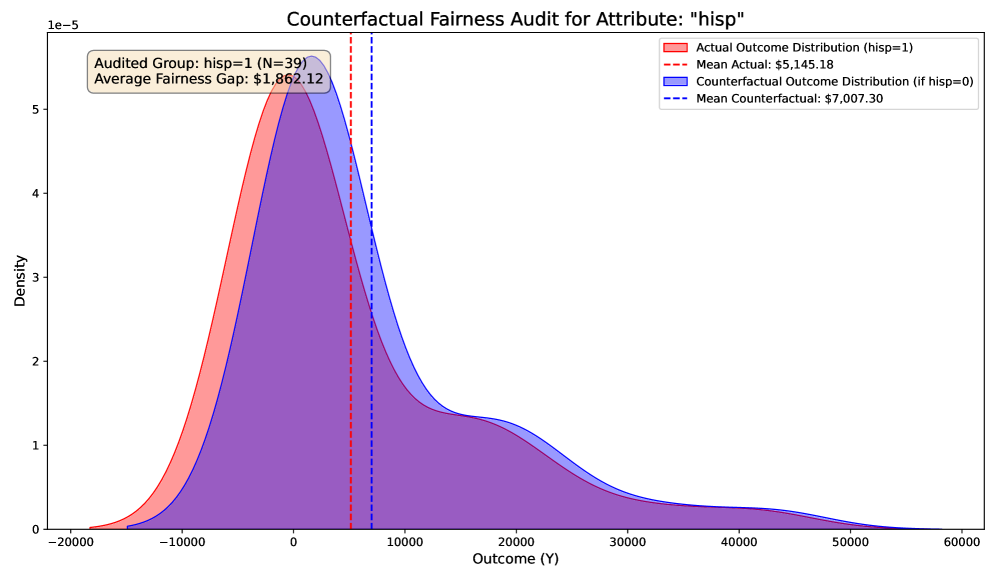

Heterogeneity Analysis: Conditional ATE (CATE).